Most neobanks have already deployed an AI agent. Far fewer have a programme that resolves beyond the “easy half” of the customer support queue. AI agents at neobanks tend to go live quickly because your stack is modern and your team moves fast, but resolution plateaus around 60% while inbound volume keeps climbing and the outbound backlog piles up.

To deploy AI agents for neobanks that clear that ceiling, supports growth, and meaningfully reduces the need for new headcount, you need the right AI vendor and a plan for deployment that aims to address the big picture, not just the easy resolutions. This guide breaks the work into five clear steps so your neobank’s AI agent deployment works out of the gate and returns value faster

1. Where to deploy AI agents for neobanks first

A generic AI agent answers a question and closes the conversation. It handles "what's my limit?" or "how do I order a new card?" well enough, but at a neobank it tends to plateau around 60% automation, because most of the queue doesn't fit the one question, one answer shape.

The work that decides your cost base sits a layer deeper. Take a disputed transaction: a customer flags a charge they don't recognise, the case opens against card-scheme reason codes, evidence gets gathered, a decision gets made, the chargeback gets submitted, and someone closes the loop weeks later, against the regulatory and scheme deadlines in every market you operate in. Collections, complaints, KYC, and bereavement run the same way: long processes, not quick replies.

So the first decision is depth, not which vendor. A specialist agent is worth more to a neobank on three fronts:

It runs the long process, not just the reply: disputes, collections, and KYC need intake, investigation, decision, follow-up, and close. A specialist agent carries memory and context across every stage. A generic agent's case stops at the first response.

Compliance is built in: in finance a wrong answer can be a regulatory breach, so the controls have to run on every turn, not sit in a settings page you maintain yourself.

It acts inside your systems: freezing a card, checking account status, or submitting a chargeback means connecting to core banking, your CRM, and case management, not just explaining the next step.

Pick the first process by pain, not by ease. Which queue is growing fastest, eats the most agent hours, and follows clear enough rules to hand over? Back-office work like disputes, collections, and KYC is usually the best first bet: high volume, defined procedures, and the part a generic bot never touched. Our guide to AI use cases in banking maps the options by effort and impact.

2. Move fast without outrunning compliance

Speed is the neobank advantage and the neobank trap. You can have an agent live in weeks, but you're still as regulated as any bank: FCA Consumer Duty in the UK, Reg E and Reg Z in the US, PSD2 and the EU AI Act in Europe. A generic bot that moves fast and mishandles a vulnerable customer turns a quick win into a regulatory incident.

The fix is controls that are the platform's job, not yours. Gradient Labs runs two kinds of guardrails on every turn:

Customer guardrails read the conversation and act on it: detecting a complaint, spotting signs of financial difficulty or vulnerability that trigger consumer-protection obligations, and handing off to a person when one is needed.

Agent guardrails check what the agent is about to say or do: blocking unlicensed advice, preventing tipping-off on a financial crime case, and stopping sensitive data from leaving. They edit the draft before it reaches the customer.

Gradient Labs runs 20+ pre-built financial services guardrails on every turn, with coverage across US, UK, and EU rules, and every action, data point, and decision lands in an audit trail your risk team can review. It also shortens the one sign-off you do still need: a lean risk function says yes faster when the guardrails and the audit trail are already there to inspect.

3. Teach the agent what your best people already know

An agent knows what you give it, and a knowledge base on its own is never enough. You hired fast to keep up with growth, and a lot of what your best people know never made it into a document: the edge cases, the workarounds, the way a sensitive complaint actually gets handled. Three sources feed the agent:

Knowledge base: your help articles and policies, the documented baseline.

Facts: the structured details that don't sit in a public article, like fee schedules, limits, and cut-off times. They're precise and they change often, so they're kept separate.

Notes: your team's working knowledge, the judgement that never got written down. Gradient Labs generates this for you, analysing thousands of conversations your team has already handled to surface how they work: the recurring edge cases, the tone they use with a vulnerable customer, and the steps they take when a policy doesn't quite fit. Your team reviews what it finds, and it becomes guidance the agent applies from day one.

On top of knowledge sit procedures: your SOPs written as natural-language steps the agent runs, with branching for the cases that don't follow the script. Because the agent learns from your real conversation history, it starts near your team's standard instead of climbing to it over months. Treat early gaps the way you would a new hire: a poor answer signals missing context, not a dead end.

4. Plug into your modern stack

This is where the neobank advantage is real. You built on APIs, your systems talk to each other, and you don't have a thirty-year-old core to wrestle. An agent earns its return when it can act: freeze a card, check account status, take a payment, update a case. For a neobank, wiring it into core banking, your CRM, and case management is faster than it is for an incumbent, so use that lead.

Sequence the integrations the way you sequenced the processes. Connect what unblocks your highest-volume case first, then widen. This is also where the economics turn. Most of the saving arrives past 80% automation, and the climb from 60% to 80% is mostly integration depth: every system the agent can reach is another case it closes without a human. Overdue payment collections is the plain example, since the agent can't resolve the case if it can't see the balance and take the payment. Start with one process, then add others on the same connections, guardrails, and audit trail.

5. How to deploy AI agents for neobanks that keep up with growth

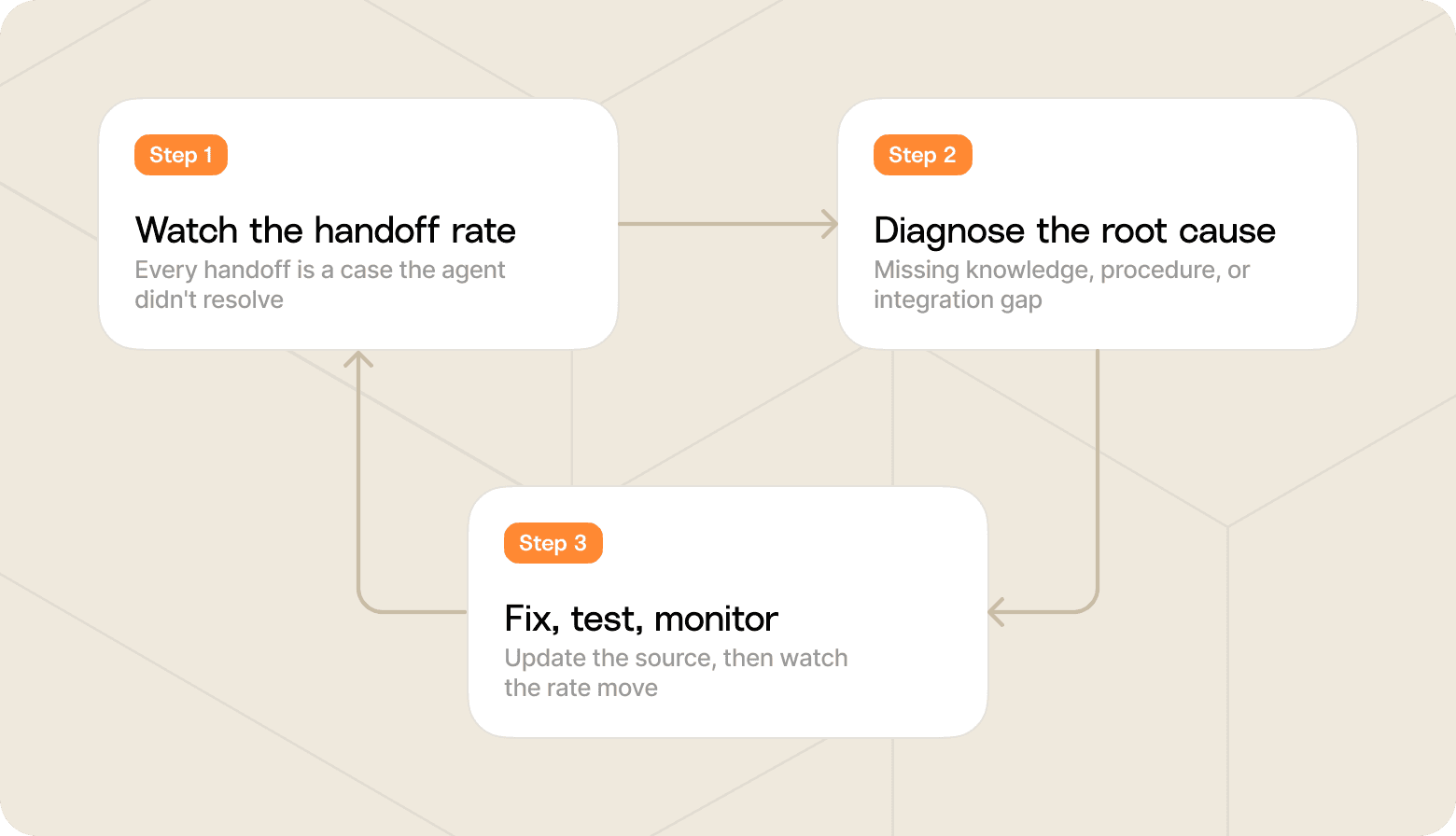

Going live is the start line. A mature deployment reaches 80 to 90% resolution, but day one usually lands around 60%, and you close the gap with a loop you run after launch:

Watch the handoff rate: every handoff to a human is a case the agent didn't resolve.

Diagnose the root cause: missing knowledge, a gap in a procedure, or a missing integration.

Fix the source, then test and monitor: update the knowledge, procedure, or tool, validate it, and watch the rate move.

For a neobank the ramp matters more than for anyone, because your volume doesn't wait. A large digital bank running Gradient Labs started at 50 tickets a day with 100% human QA, moved to 25%, 50%, and 100% of email volume as the numbers held, and never rolled back. When 30,000 new accounts landed overnight and support volume tripled in a week, the agent absorbed it. It now holds 98% QA across half a million conversations and an 84% CSAT, ahead of its human team.

That's the pattern that defines a neobank deployment: growth absorbed without headcount added behind it. Pockit, a mobile-first consumer fintech, went live in three weeks and reached a 70% resolution rate with an 80% lift in CSAT. As their Head of Operations, Michiel Smet, put it: "With Gradient Labs, we have an AI agent that's actually solving problems, boosting our CSAT rating, and absorbing growth without us having to scale the team." Plum hit 52% resolution on day one and climbed from there.

Deployment is the hard part, and it's the part Gradient Labs is built to carry: an FS-native platform, a delivery team that knows financial services, and a guarantee on every use case we scope. If you're mapping where to start, our guide to taking an AI agent from pilot to production walks the sequence, or book a demo and we'll plan your first deployment.

Elizabeth Shew leads Brand and Advocacy at Gradient Labs, where AI agents handle customer support and back-office work for banks, lenders, and fintechs. Before that, she led customer marketing at Mastercard and built Dynamic Yield's customer marketing programme from the ground up, a decade spent turning customer results into industry-shaping stories. She writes about how support and operations teams actually put AI and technology to work. Before tech, she was a professional dancer in NYC.