What is back office AI?

Back office AI covers the AI agents and automation platforms that run the work behind a financial services operation rather than the work in front of the customer: verifying who someone is, investigating a suspicious transaction, processing a dispute, or moving a loan application toward a decision. It sits next to, and increasingly inside, the systems that already run KYC, AML, collections, and lending.

Most of these AI agent companies specialise in one job. A KYC platform verifies identity and onboards a customer. An AML platform watches transactions for financial crime. A lending platform moves an application through underwriting. Few run more than one of these jobs, and fewer still also run the customer-facing conversation that triggers or follows the back-office work, which is the gap this guide's first entry, Gradient Labs, is built to close.

This guide ranks 13 platforms across that back-office scope: customer service automation, KYC verification, dispute resolution, financial crime, and lending workflows.

Platform | Best For | Pricing | Channels |

|---|---|---|---|

Gradient Labs | End-to-end operations for regulated finance | Per-resolution, with a deployment guarantee | Chat, email, and voice |

Fenergo | Client lifecycle management and KYC for large, multi-business-line banks | Custom enterprise, demo-gated | Not applicable (back-office only) |

WorkFusion | Scaling AML and sanctions alert review without adding headcount | Custom enterprise, demo-gated | Not applicable (back-office only) |

ComplyAdvantage | AML and KYC screening across multiple jurisdictions | Tiered (Starter, ComplyLaunch); rates not public | Not applicable (back-office only) |

Bretton AI | Automating financial-crime investigations end to end | Custom enterprise | Not applicable (back-office only) |

Sardine | Fraud, AML, and compliance on one risk platform | Custom enterprise | Not applicable (back-office only) |

Unit21 | Detection and case investigation in one loop | Custom enterprise | Not applicable (back-office only) |

Hawk | Transaction monitoring you can explain to a regulator | Custom enterprise | Not applicable (back-office only) |

Lucinity | Speeding up investigations without removing the analyst | Custom enterprise | Not applicable (back-office only) |

Quavo | Automating fraud claims and chargeback disputes at scale | Custom enterprise | Not applicable (back-office only) |

Casca | Modernising business and SBA loan origination | Custom enterprise | Not applicable (back-office only) |

Parlay | Widening the SBA lending funnel | Custom enterprise | Not applicable (back-office only) |

Oscilar | One risk-decisioning layer across fraud, compliance, and credit | Custom enterprise | Not applicable (back-office only) |

Methodology: how we evaluated these platforms

Four factors decide where a back office AI platform lands on this list:

Resolution depth: does the platform close the case (a verified identity, a closed investigation, a submitted chargeback) or does it stop at a flag, a score, or a single reply?

Action capabilities: can the platform act inside the systems of record (updating a case, submitting a filing, taking a payment), or does it only surface information for a human to act on?

Channel coverage: for any platform that touches the customer, does it run chat, voice, and email, or one channel only?

Pricing transparency: does the vendor publish a pricing model a buyer can evaluate against their own volume, or is pricing demo-gated?

Vendors for AI customer service, KYC, KYB, disputes, collections, and lending:

1. Gradient Labs: best for end-to-end operations in regulated finance

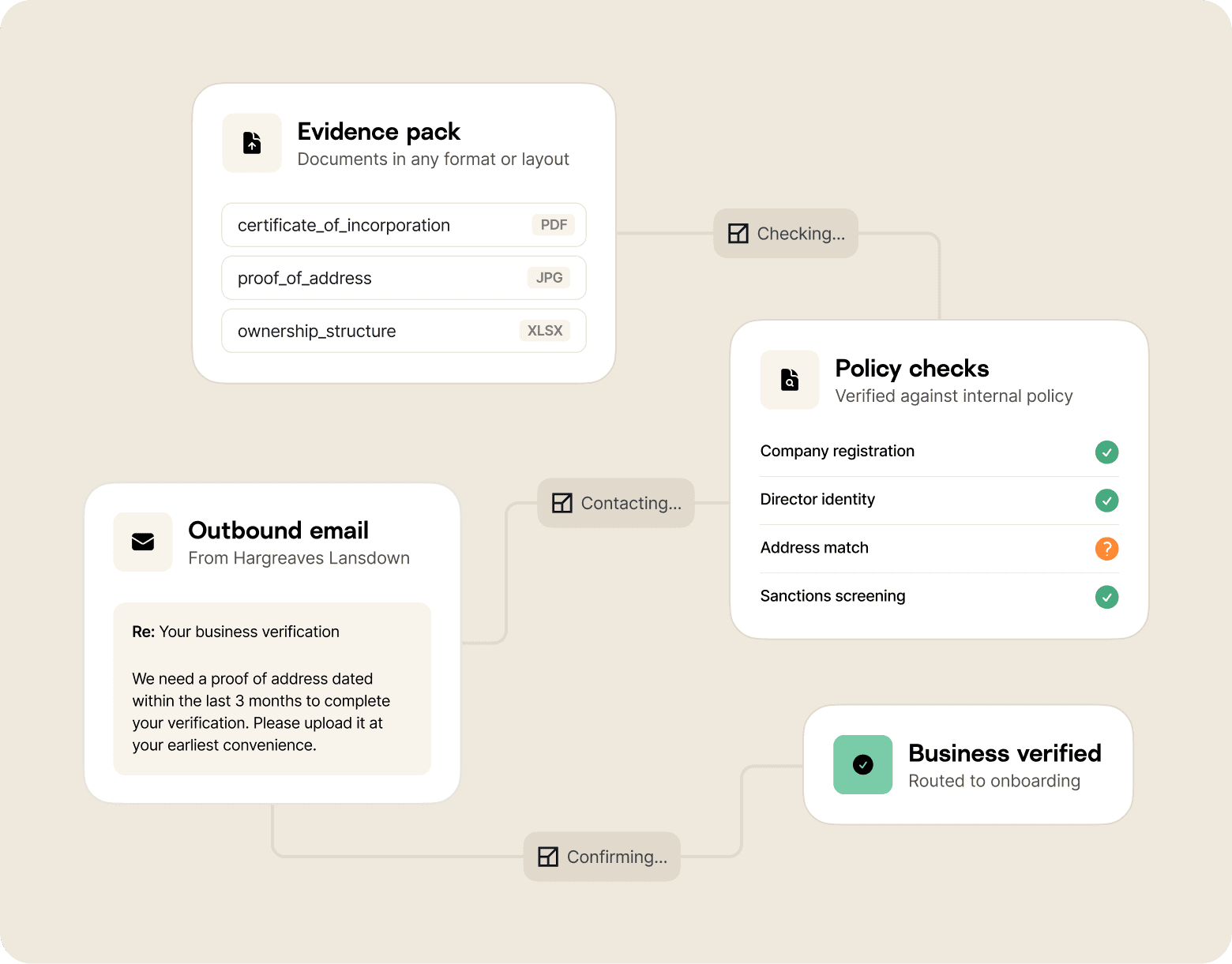

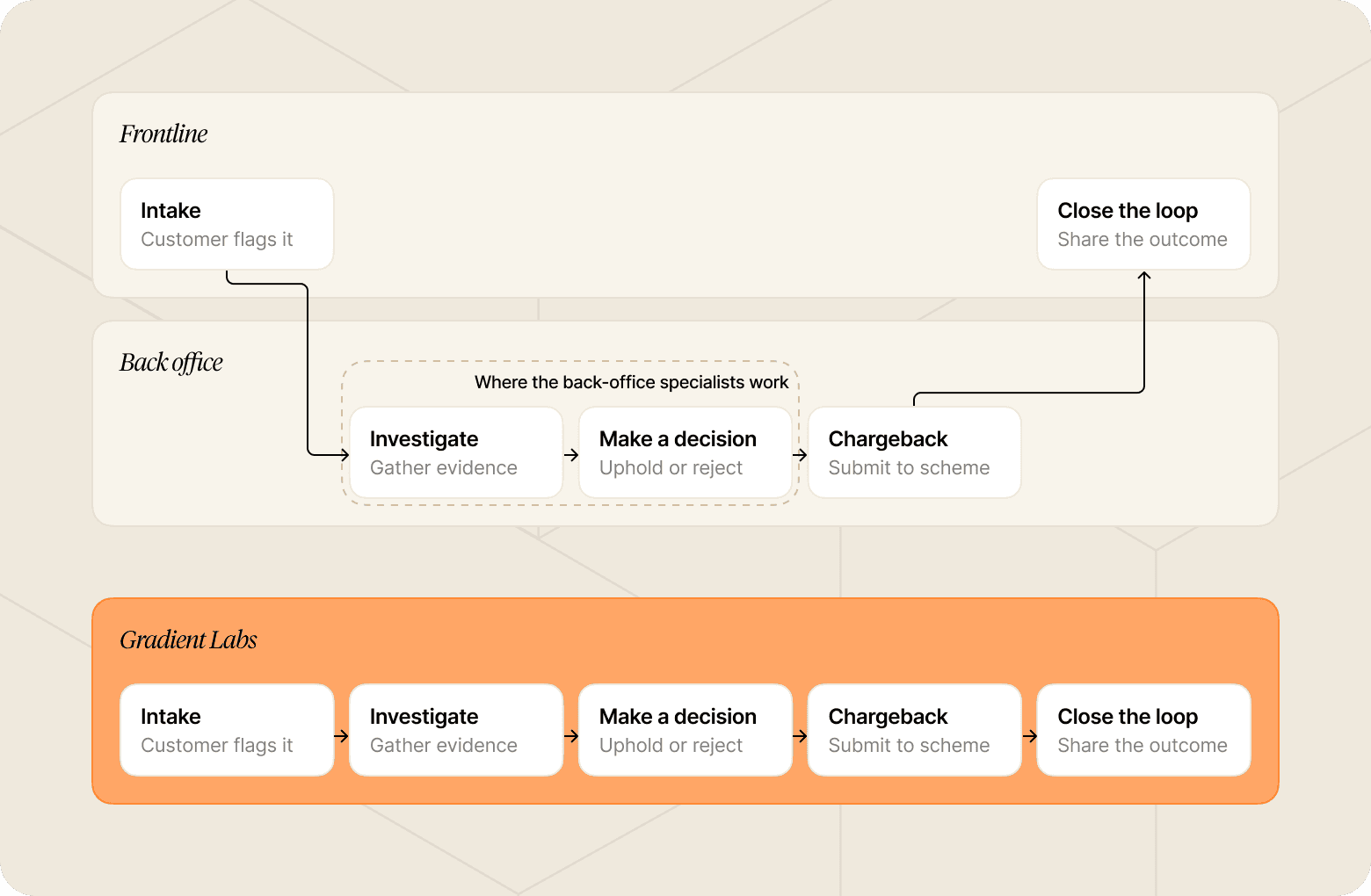

Gradient Labs runs customer operations end to end: the customer-facing conversation and the back-office case work behind it, together on one platform. A disputed transaction starts on the frontline, runs investigation and chargeback work in the back office, and closes back out with the customer, and Gradient Labs holds that case end to end rather than handing it across a gap between tools.

Regulated-operations proof points:

SOC 2 Type II certified

20+ pre-built financial services guardrails running on every turn

Regulatory coverage across FCA Consumer Duty and CONC in the UK, FDCPA and TCPA in the US, and GDPR and the EU AI Act

Full audit trail of every agent action, data point, and reasoning step

Zero-day data retention agreements with every LLM sub-processor

Key features:

Runs the full KYC process end to end: chasing outstanding or rejected documents, conducting enhanced due diligence, and keeping verification moving until every customer is cleared or flagged for compliance review

Specialist agents for KYC, disputes, and lending that share memory and context across the customer lifecycle

Guardrails that read the conversation itself: rerouting when a customer shows signs of vulnerability or financial difficulty, and editing a reply before it sends if it strays into tipping-off, a false promise, or out-of-bounds advice

A finserv-native AI delivery team that runs the 0 to 1 migration so a non-technical ops lead can own the agent

Voice AI in production at scale, a first in finance

A deployment guarantee: money back if a scoped use case isn't delivered

Pricing: Per-resolution, with a deployment guarantee.

Best for: Banks, lenders, and fintechs running customer service automation and back-office work like KYC, disputes, and lending, including collections, on one platform.

"We truly think that if people have a problem and you solve it, that builds brand loyalty. That's why customer resolution is so important. With Gradient Labs, we have an AI agent that's actually resolving problems, boosting our CSAT rating, and absorbing growth without us having to scale the team. I'm confident that with this partnership, we can get to 100% automation."

Michiel Smet, Head of Operations, Pockit

Another customer, Plum, has deployed our AI agent with a 98.6% QA score, evidence that the quality holds even where headcount and engineering effort stay low.

2. Fenergo: best for client lifecycle management and KYC at large banks

Fenergo runs a client lifecycle management (CLM) platform with AI agents, branded KYRA, that move KYC from a periodic review into continuous monitoring. It serves corporate and institutional banking, commercial banking, asset management, private banking, and energy and commodities trading, with partnerships across Salesforce, AWS, Deloitte, PwC, LSEG, and Moody's.

Key features:

Continuous KYC monitoring rather than periodic refresh cycles

Client onboarding and identity verification workflows

Transaction monitoring tied to the client record

Coverage across corporate, institutional, private banking, and energy and commodities clients

Integration partnerships with major banking and data providers

Pricing: Custom enterprise, demo-gated. No public pricing page.

Best for: Large banks running complex KYC across multiple business lines.

3. WorkFusion: best for scaling AML alert review

WorkFusion runs AI agents for AML and sanctions compliance, performing Level 1 alert reviews and Level 2 investigations so a compliance team can scale screening volume without adding headcount. It's used by 10 of the top 20 banks globally and holds SOC 2 Type II certification.

Key features:

Level 1 and Level 2 AML alert review and investigation

Sanctions screening and adverse media monitoring

Transaction monitoring and fraud detection

Documented, explainable decisions built for regulator review

SOC 2 Type II certified

Pricing: Custom enterprise, demo-gated. No public pricing page.

Best for: Compliance teams scaling AML and sanctions screening without adding headcount.

4. ComplyAdvantage: best for AML and KYC across multiple jurisdictions

ComplyAdvantage runs an AI-native risk intelligence platform, Mesh, covering customer screening, company screening, transaction monitoring, and payment screening. Its agentic workflows are built to resolve routine alerts autonomously while keeping the decision regulator-defensible.

Key features:

Customer, company, and payment screening in one platform

Ongoing monitoring rather than point-in-time checks

Agentic workflows aimed at routine alert resolution

Global intelligence data feeding the risk decision

Tiered plans (Starter, ComplyLaunch) for teams scaling into new jurisdictions

Pricing: Tiered (Starter, ComplyLaunch); exact rates not public.

Best for: Compliance teams running AML and KYC screening across multiple regulatory jurisdictions.

5. Bretton AI: best for automating financial-crime investigations

Bretton AI, formerly Greenlite, builds AI agents for AML, KYC/KYB, and sanctions investigations that produce an investigation-ready conclusion an analyst can sign off, rather than a black-box score. It raised a $75M Series B in February 2026 led by Sapphire Ventures and counts Robinhood, Mercury, Gusto, and Lead Bank as customers.

Key features:

Agentic AML, KYC/KYB, and sanctions investigation

Ongoing transaction monitoring

Investigation-ready conclusions built for analyst sign-off

$95M total funding as of its 2026 Series B

Customers including Robinhood, Mercury, and Gusto

Pricing: Custom enterprise. No public pricing page.

Best for: Banks and fintechs automating financial-crime investigations end to end.

6. Sardine: best for fraud, AML, and compliance on one platform

Sardine runs fraud, AML, and compliance on a single risk platform and has moved into agentic investigation that gathers evidence and interprets context across a case. It has raised $145M to date and serves more than 300 companies, including FIS, Deel, and GoDaddy.

Key features:

Fraud, AML, and compliance under one platform

Agentic investigation that gathers and interprets case evidence

Device and behavioural risk signals feeding the decision

300+ customers across payments, banking, and crypto

$145M raised to date

Pricing: Custom enterprise. No public pricing page.

Best for: Teams that want fraud, AML, and compliance under one risk platform rather than three tools.

7. Unit21: best for detection-to-investigation in one loop

Unit21 runs an agentic fraud and AML platform where detection and investigation sit in the same loop, with the agent showing its work. It has raised around $92M, most recently a $45M Series C, and is used by 200+ institutions including Intuit, Chime, and Sallie Mae.

Key features:

Agentic fraud and AML detection through investigation

Case management built around the same data as detection

Used by 200+ institutions

Named to the 2026 RegTech100

Configurable rules alongside agentic review

Pricing: Custom enterprise. No public pricing page.

Best for: Risk operations teams that want detection and case investigation in one place.

8. Hawk: best for explainable transaction monitoring

Hawk uses explainable AI for AML transaction monitoring and sanctions screening, with automated SAR drafting and a focus on cutting false positives, since a monitoring decision has to survive a regulator's question about why it fired. The Munich-based company raised a $56M Series C in 2025 and works with 80+ institutions, including Synctera.

Key features:

Explainable AML transaction monitoring

Sanctions screening alongside monitoring

Automated SAR drafting

False-positive reduction as a stated design goal

80+ institutions served, from Tier 1 banks to fintechs

Pricing: Custom enterprise. No public pricing page.

Best for: Banks modernising transaction monitoring without losing auditability.

9. Lucinity: best for analyst-led investigations

Lucinity's FinCrime agents, branded Luci, compress investigations from hours to minutes while keeping a human analyst in control of the decision. The Iceland-based firm has raised $26M to date and counts Pleo and Visa's Currencycloud among its customers.

Key features:

FinCrime investigation copilot built around analyst review

Investigation time compressed from hours to minutes

Human-in-control decision model

Case narrative generation for analyst sign-off

Customers including Pleo and Visa Currencycloud

Pricing: Custom enterprise. No public pricing page.

Best for: FinCrime teams that want an agent working alongside analysts, not instead of them.

10. Quavo: best for automating fraud claims and chargeback disputes

Quavo's QFD dispute management platform automates fraud claim intake, chargeback management, and dispute resolution for issuing banks, credit unions, and fintechs. It has recovered $1.83 billion for 13.6 million fraud victims and processes over a million disputes a month, with resolutions landing 28 days faster than the industry average.

Key features:

Automated fraud claim intake and chargeback management

90% task automation in a published First Hawaiian Bank case study

SOC 2 Type 2, SOC 1 Type 1, and PCI DSS compliance

Over a million disputes processed monthly across its customer base

Customers including USAA, KeyBank, and Green Dot

Pricing: Custom enterprise. No public pricing page.

Best for: Issuing banks and fintechs automating fraud claims and chargeback disputes at scale.

11. Casca: best for AI-native loan origination

Casca, built by Cascading AI, runs an AI-native loan origination system used by FDIC-insured banks and fintechs, with a strong line in small-business and SBA lending. It raised a $29M Series A led by Canapi Ventures, with customers including Live Oak Bank and Huntington National Bank.

Key features:

AI-native loan origination workflow

Strong focus on small-business and SBA lending

Used by FDIC-insured banks and fintechs

$33M total funding raised

Customers including Live Oak Bank and Huntington National Bank

Pricing: Custom enterprise. No public pricing page.

Best for: Banks and lenders modernising business and SBA loan origination.

12. Parlay: best for widening the SBA lending funnel

Parlay runs a loan-readiness agent that pre-qualifies and packages applications so more of them reach a decision rather than stalling at the top of the funnel. The seed-stage company, backed by JAM FINTOP, works with community banks and credit unions on SBA loan volume.

Key features:

Loan-readiness pre-qualification and packaging

SBA lending focus

Built for community banks and credit unions

Backed by JAM FINTOP

Aimed at applications that would otherwise stall before reaching underwriting

Pricing: Custom enterprise. No public pricing page.

Best for: Community lenders widening the top of the SBA funnel without adding headcount.

13. Oscilar: best for a unified risk-decisioning layer

Oscilar runs an AI agent hub spanning fraud, AML compliance, credit risk, and onboarding, used across 100+ financial institutions. Founded by Apache Kafka co-creator Neha Narkhede, it is bootstrapped with no outside funding and counts SoFi, MoneyGram, and Nuvei among its customers.

Key features:

One platform across fraud, AML, credit risk, and onboarding

Used by 100+ financial institutions

Bootstrapped, no outside funding

Customers including SoFi, MoneyGram, and Nuvei

Built by a team with prior large-scale data infrastructure experience

Pricing: Custom enterprise. No public pricing page.

Best for: Institutions that want one risk-decisioning layer across fraud, compliance, and credit rather than separate tools per risk type.

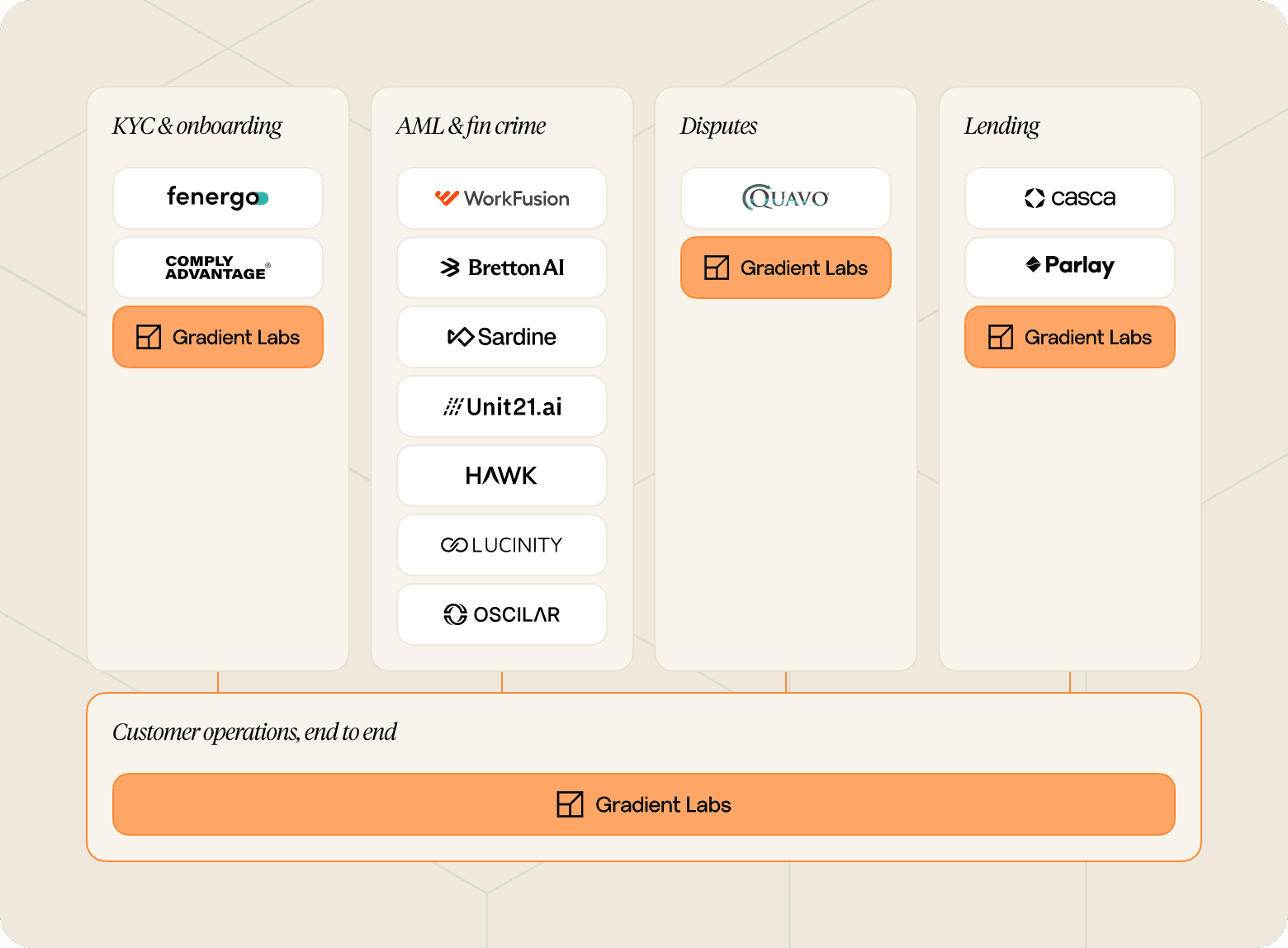

How these platforms fit together

Most banks and lenders run more than one of these platforms at once, because each owns a different job. KYC and onboarding (Fenergo, ComplyAdvantage) clear a customer before they transact. AML and financial crime tools (WorkFusion, Bretton AI, Sardine, Unit21, Hawk, Lucinity, Oscilar) sit downstream of that moment, screening the transactions and the entities behind them. Quavo runs the dispute when something goes wrong. Casca and Parlay move a lending application toward a decision. Gradient Labs is the one platform that runs the customer-facing conversation underneath all of it, and the hardship and forbearance case work that follows.

The practical question for most buyers isn't which single platform wins. It's which platform owns each job, and whether the customer-facing layer holding them together actually closes the loop with the customer or stops at a handoff. For a deeper look at what to check before picking a vendor, see our guide on how to choose an AI agent vendor for financial services.

If your evaluation is narrower, customer service automation specifically rather than the full back-office stack, our Intercom Fin vs Gradient Labs comparison goes deeper on that specific decision.

Book a demo to see how Gradient Labs runs end-to-end operations on your own use case.