Picking a secure AI agent for banking is a security decision as much as a customer-experience one. AI agents in banking read balances, move money, investigate financial crime, and handle vulnerable customers, so each one has to clear risk, compliance, and infosec review before it goes near a customer or a case. The bar rises when regulation treats the work as high-risk: the EU AI Act classifies credit scoring and creditworthiness checks as high-risk uses. This guide ranks the best secure AI agents for banking across the three jobs where AI in banking now runs on agents: customer service and operations, financial crime and risk, and lending.

Who is the best secure AI agent for banking in 2026?

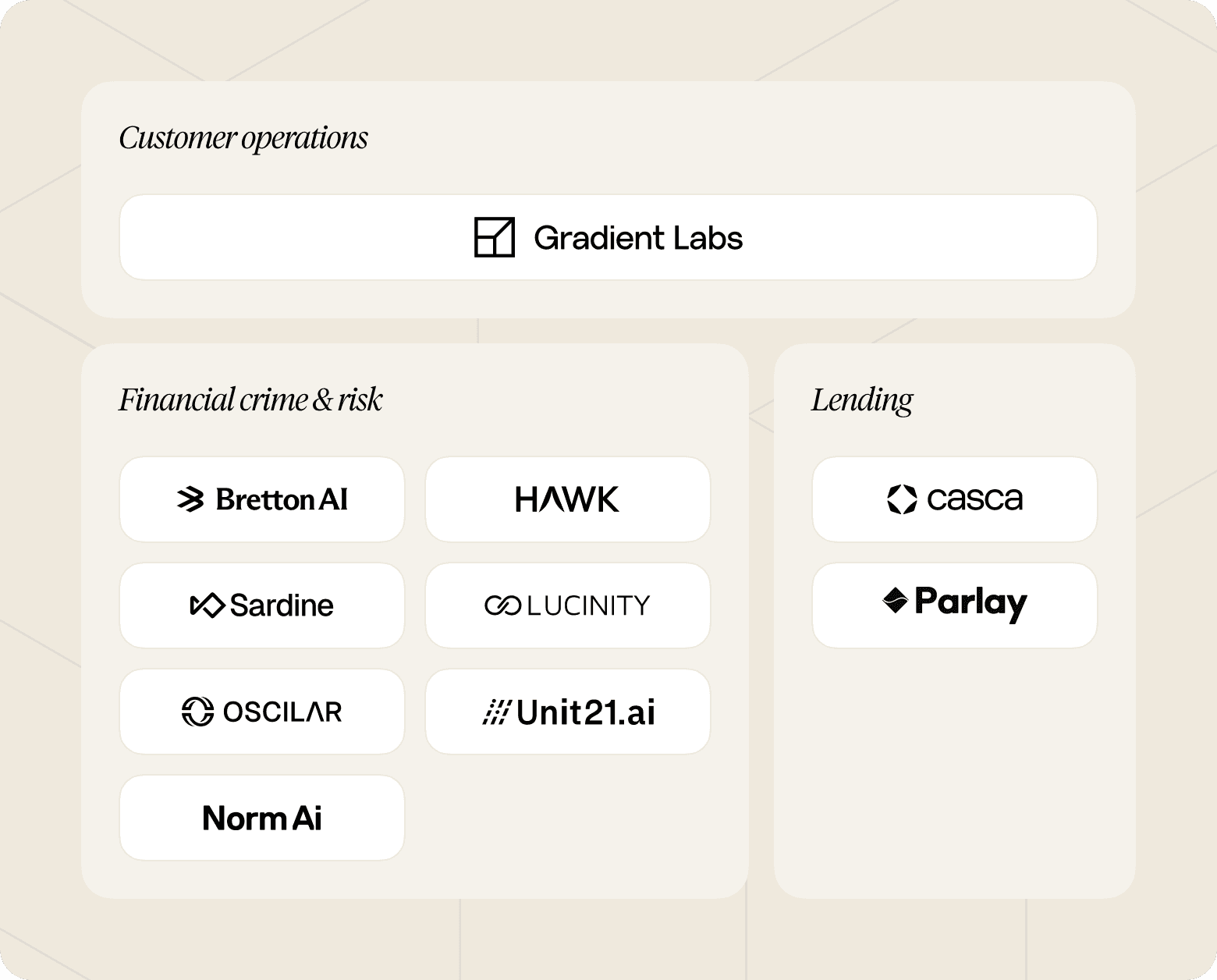

Gradient Labs is the standout for banks, fintechs, lenders, and credit unions that need a secure AI agent across customer operations, because it runs frontline support and back-office work like disputes, collections, and KYC on one platform, with guardrails on every turn and coverage across US, UK, and EU regulation. Around that sits a strong field of FS-specific agents, each owning a different part of the bank: Bretton AI, Sardine, Unit21, Hawk, Lucinity, Norm Ai, and Oscilar for financial crime and risk, and Casca and Parlay for lending. Most banks will run more than one, so the useful question is not which single agent wins, but which one owns each job.

Platform | What it does | Where it fits in the bank | Compliance posture | Best for |

|---|---|---|---|---|

Gradient Labs | Frontline and back-office customer operations (disputes, collections, KYC) | The customer-facing layer and the case work behind it | 20+ FS-native guardrails every turn, SOC 2 Type II, US/UK/EU coverage | Banks running frontline and back-office customer operations work on one platform |

Bretton AI (formerly Greenlite) | Agentic AML, KYC/KYB, and sanctions investigations | Financial-crime back office | Audit-ready agents, FS-built compliance focus | Automating financial-crime investigations |

Sardine | Fraud, AML, and compliance with agentic investigation | Fraud and FinCrime | FS-built risk platform | Fraud, AML, and compliance on one risk platform |

Unit21 | Agentic fraud and AML, detection through investigation | Fraud and AML operations | Human-readable audit trail, 2026 RegTech100 | Detection and case investigation in one place |

Hawk | AML monitoring and sanctions screening on explainable AI | Transaction monitoring | Explainable AI, automated SAR drafting | Modernising transaction monitoring |

Lucinity | FinCrime investigation agents working alongside analysts | The FinCrime analyst desk | Human-in-control copilot model | Speeding up investigations without removing the analyst |

Norm Ai | Regulatory agents that encode laws and policy into checks | Compliance and legal | Regulation encoded into automated review | Operationalising regulatory requirements |

Oscilar | AI agent hub across fraud, AML, credit risk, and onboarding | Risk-decisioning layer | Used across 100+ financial institutions | One risk layer across fraud, compliance, and credit |

Casca | AI-native loan origination for business and SBA lending | Lending front office | Used by FDIC-insured banks | Modernising loan origination |

Parlay | Loan-readiness agent that pre-qualifies and packages applications | Lending top of funnel | SBA-focused | Widening the lending funnel |

What makes a secure AI agent for banking?

A secure AI agent for banking has to do more than encrypt data in transit. Use these five criteria to evaluate any vendor, and see our more detailed guide to choosing an AI agent vendor for financial services for more depth.

Regulatory coverage across your markets: US rules (FDCPA, TCPA, Reg F, UDAAP), UK rules (FCA Consumer Duty, CONC, Breathing Space), and EU rules (GDPR, EU AI Act) differ. An agent built around one market cannot safely run another.

Guardrails and human oversight on every turn: the agent should catch the risky moments before they reach a customer or a filing, and hand the call back to a human where regulation demands it.

A full audit trail: every action, data point, tool call, and reasoning step has to be logged for the work to survive a regulator or an internal risk review.

Data security you can hand to infosec: SOC 2, encryption at rest and in transit, and zero-day data retention with every LLM sub-processor are the floor.

Real work, not just a flag: a strong agent completes the case, the investigation, or the application, rather than raising an alert and leaving the work on a human's desk.

Customer operations: the agent that runs the conversation and the case

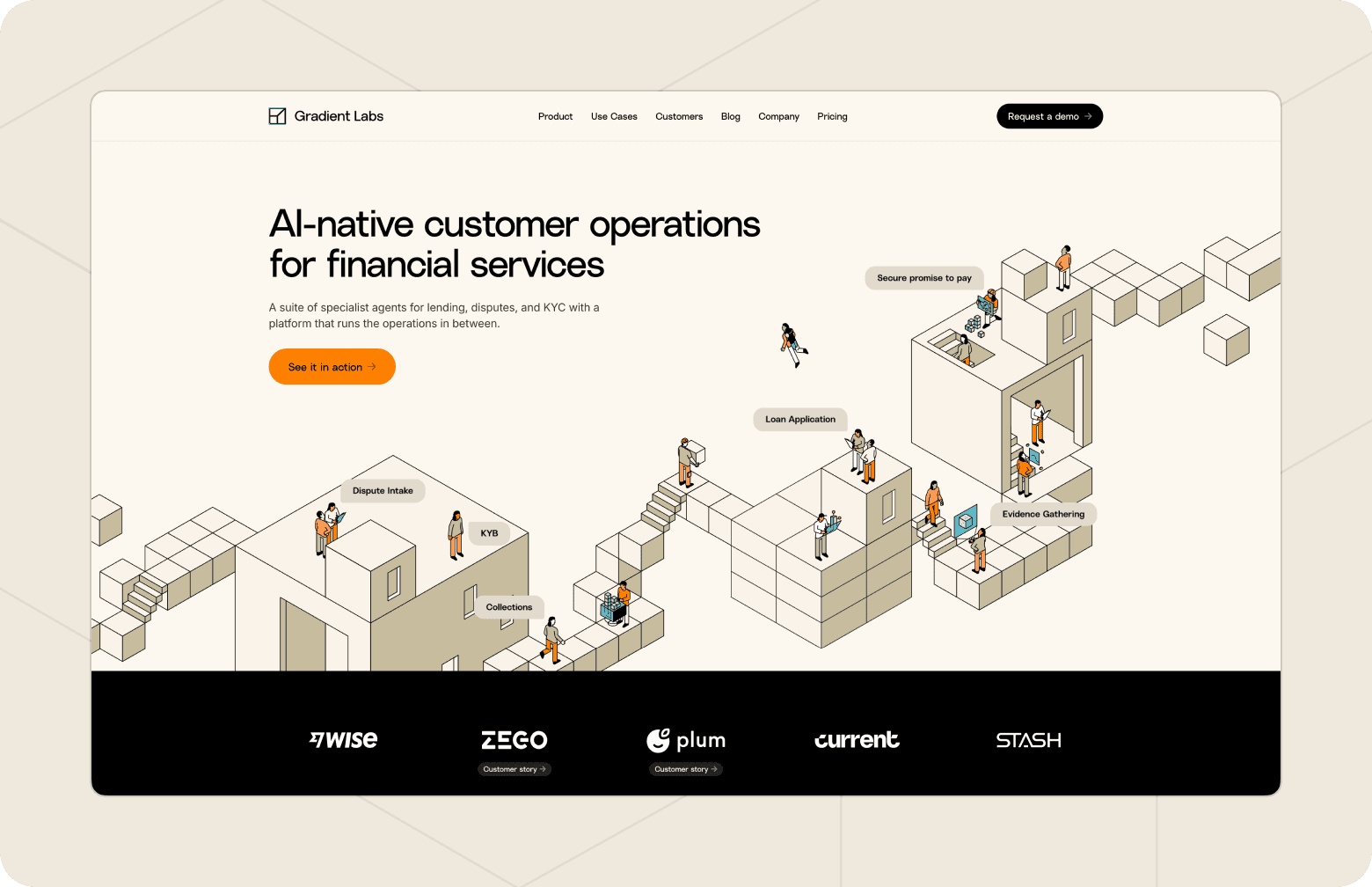

1. Gradient Labs: best for end-to-end banking operations

Gradient Labs is the AI customer service platform for financial services, and the leading platform for customer support automation that runs both frontline conversational AI and back-office case work across one platform. It works across the breadth of financial services, fitting a traditional bank just as well as lenders, fintechs, credit unions, community banks, and insurtechs. A disputed transaction starts on the frontline, runs investigation and chargeback work in the back office, and closes back with the customer. Where Gradient Labs handles a case end to end, frontline-only and back-office-only tools hand it across a gap. Notable logos include Wise, Current, Rho, LHV Bank, Stash, Zego, and Pockit.

Security and compliance: 20+ pre-built financial-services guardrails run on every turn, with coverage across US (FDCPA, TCPA, Reg F, UDAAP), UK (FCA Consumer Duty, CONC, Breathing Space), and EU (GDPR, EU AI Act) regulation. SOC 2 Type II is certified, data is encrypted at AES-256, and there are zero-day retention agreements with every LLM sub-processor. The Vanta Trust Centre is public for due diligence.

Deployment: the finserv-native AI delivery team runs the migration from whatever you run today, so a non-technical ops lead can own the agent without staffing an AI team. Agents typically go live in days, and the deployment is backed by a money-back guarantee on any scoped use case.

Resolution: 60% from day one, climbing to 80-90% in mature deployments as the team supercharges the agent in production.

Honest limitation: Gradient Labs runs customer operations. It does not run transaction monitoring, credit decisioning, or loan origination, so it sits alongside the financial-crime and lending agents below rather than replacing them.

Best for: banks, lenders, and fintechs running frontline and back-office work where compliance is non-negotiable. See the Disputes Agent and Voice for the named work.

"Now we make 33,000 calls a month, converting 60% of engaged customers to committed repayment dates, all within FCA compliance standards. It has fundamentally changed how we manage the collections layer of our lending infrastructure."

— Violeta Filip, Head of Customer Experience, SteadyPay

Financial crime, fraud, and risk agents

Financial crime is the most established home for AI in banking, and it is now where agents are moving fastest, from pattern-matching models towards systems that gather evidence and produce investigation-ready conclusions. These seven are the standouts.

2. Bretton AI: best for agentic financial-crime investigations

Bretton AI (formerly Greenlite AI) builds audit-ready AI agents for AML, KYC/KYB, and sanctions investigations, plus ongoing transaction monitoring. It raised a $75M Series B in February 2026 (led by Sapphire Ventures) alongside the rebrand from Greenlite, and counts Robinhood, Mercury, Gusto, and Lead Bank among its customers. The agents are built to produce investigation-ready conclusions an analyst can sign off, rather than a black-box score.

Best for: banks and fintechs automating financial-crime investigations end to end.

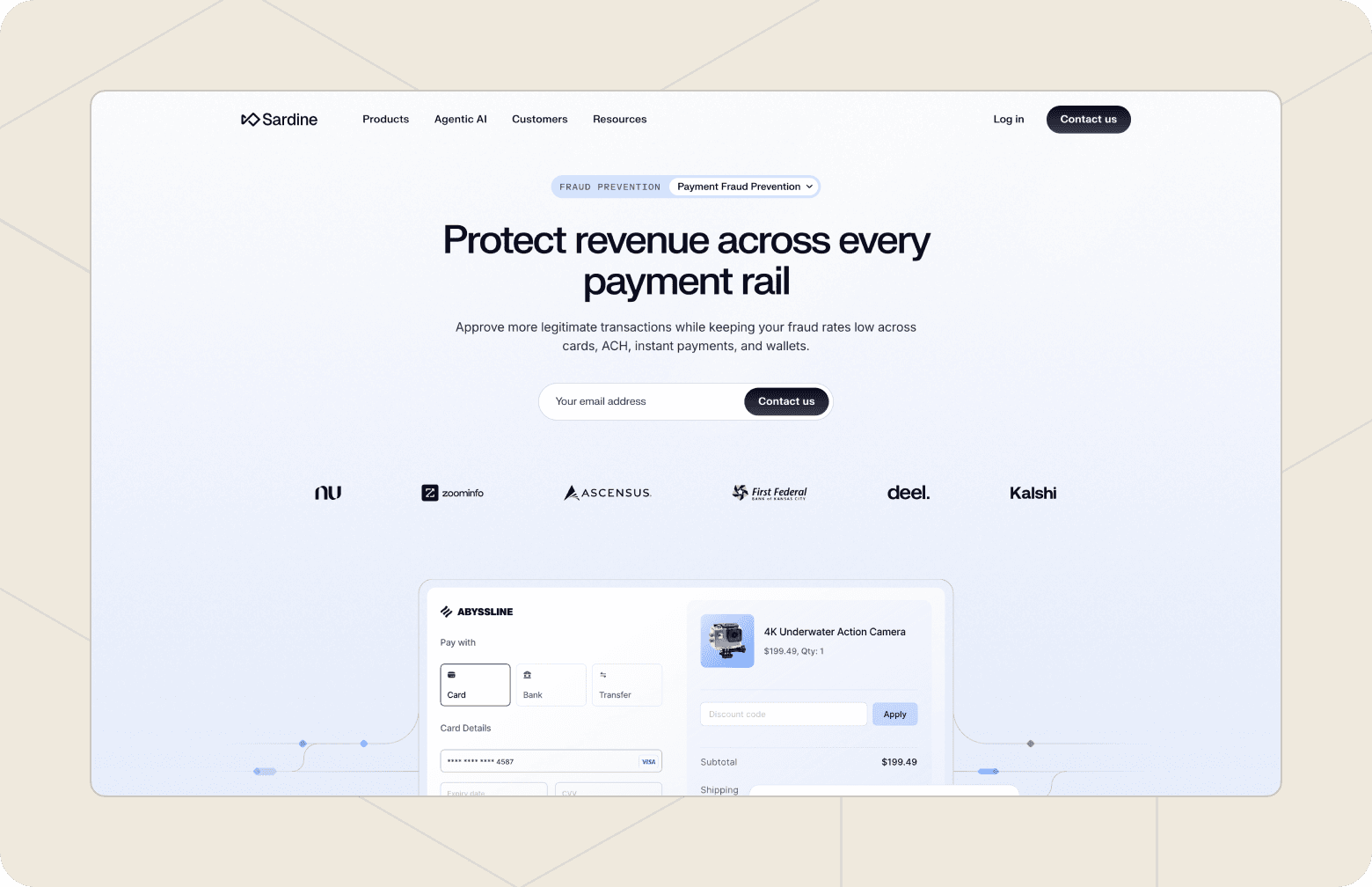

3. Sardine: best for fraud, AML, and compliance on one platform

Sardine runs fraud, AML, and compliance on a single risk platform, and has moved into agentic investigation that gathers evidence and interprets context across a case. It has raised $145M to date, including a $70M Series C in 2025, and serves more than 300 companies including FIS, Deel, and GoDaddy. It is one of the FS-stack vendors we are comfortable recommending alongside Gradient Labs.

Best for: teams that want fraud, AML, and compliance under one risk platform rather than three tools.

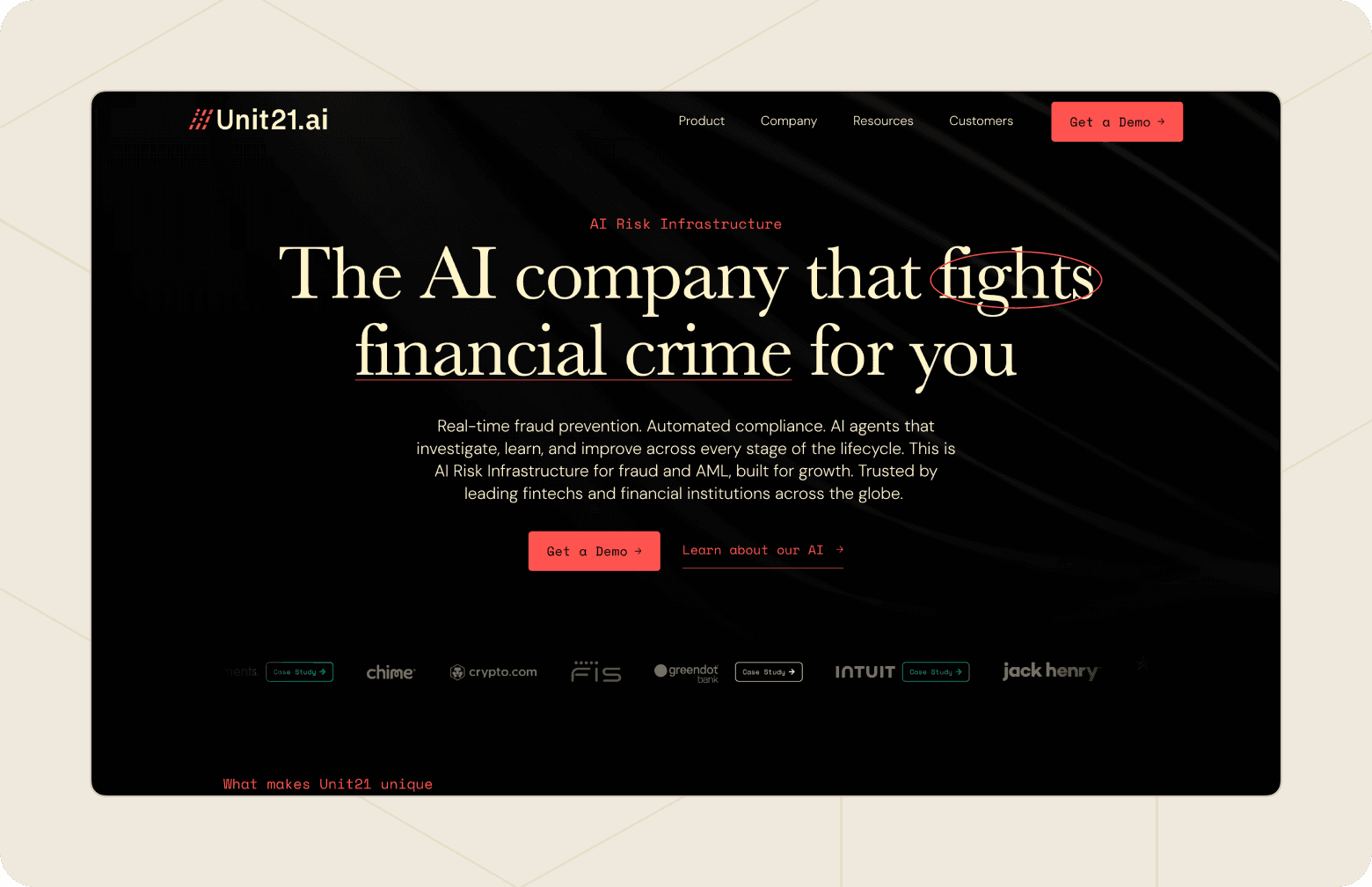

4. Unit21: best for detection-to-investigation in one loop

Unit21 runs an agentic fraud and AML platform where the agents handle the full loop from detection to investigation and show their work. It has raised around $92M (most recently a $45M Series C) and is used by 200+ institutions including Intuit, Chime, and Sallie Mae. It was named to the 2026 RegTech100.

Best for: risk operations teams that want detection and case investigation in one place.

5. Hawk: best for explainable transaction monitoring

Hawk uses explainable AI for AML transaction monitoring and sanctions screening, with automated SAR drafting and a focus on cutting false positives. Explainability matters here because a monitoring decision has to survive a regulator's question about why it fired. The Munich-based company raised a $56M Series C in 2025 ($83M total) and works with 80+ institutions, from Tier 1 banks to fintechs like Synctera.

Best for: banks modernising transaction monitoring without losing auditability.

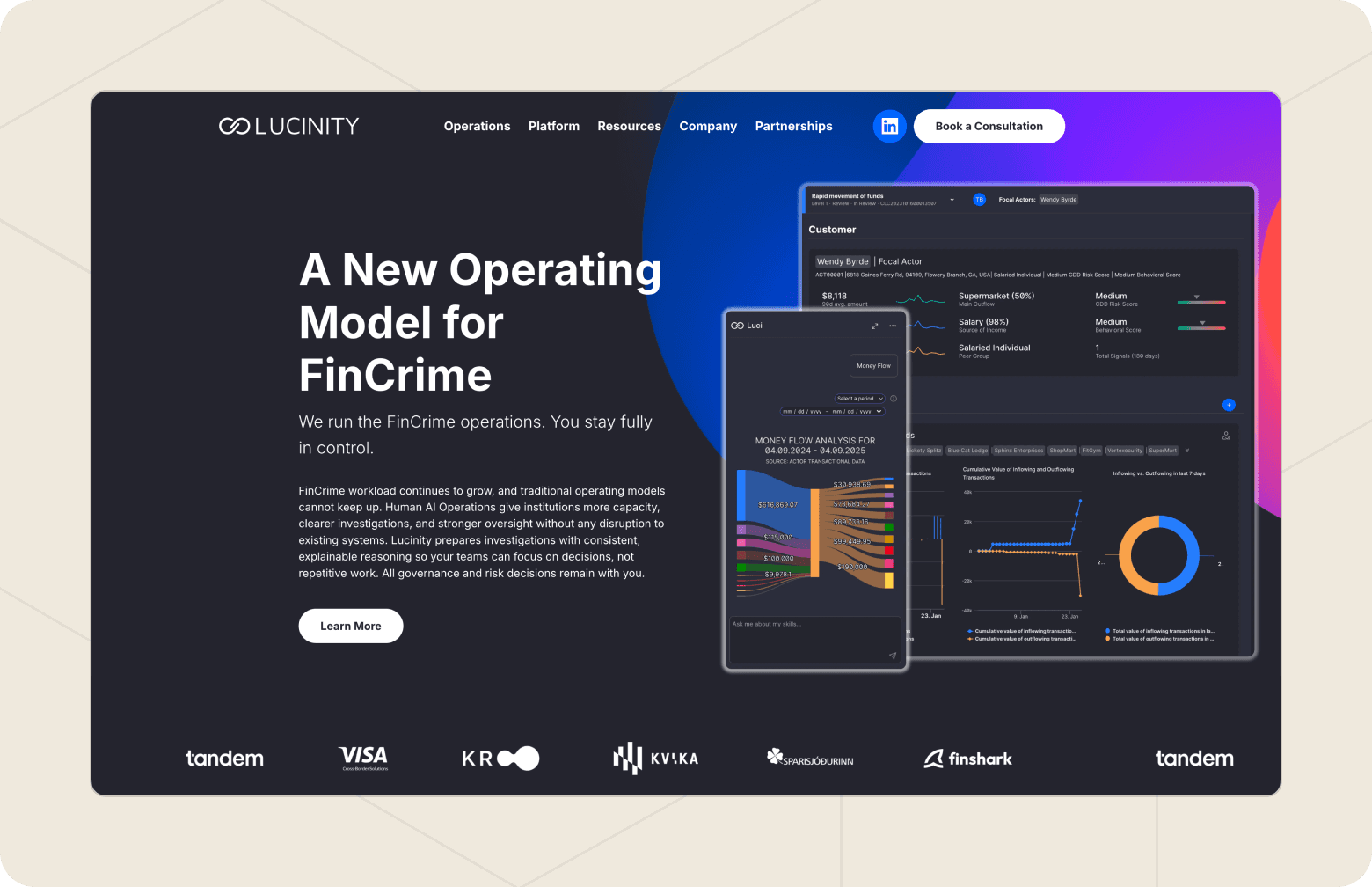

6. Lucinity: best for analyst-led investigations

Lucinity's FinCrime agents (branded "Luci") compress investigations from hours to minutes while keeping a human analyst in control of the decision. The copilot model suits teams that want speed without handing the judgement call to a machine. The Iceland-based firm has raised $26M to date and counts Pleo and Visa's Currencycloud among its customers.

Best for: FinCrime teams that want an agent working alongside analysts, not instead of them.

7. Norm Ai: best for operationalising regulation

Norm Ai builds AI agents from laws, policies, and regulatory requirements, embedding the judgement directly into compliance workflows. It is aimed at the gap between what a regulation says and what an operations team actually checks. It has raised over $140M from investors including Coatue, Bain Capital, and Citi Ventures.

Best for: compliance and legal teams turning regulatory requirements into automated checks.

8. Oscilar: best for a unified risk layer

Oscilar runs an AI agent hub spanning fraud, AML compliance, credit risk, and onboarding, used across 100+ financial institutions. Founded by Apache Kafka co-creator Neha Narkhede, it is bootstrapped with no outside funding, and counts SoFi, MoneyGram, and Nuvei among its customers. It suits institutions that want one decisioning layer rather than separate tools per risk type.

Best for: institutions that want one risk-decisioning layer across fraud, compliance, and credit.

Lending agents

Lending is the other place agents are taking on real work, from the application through underwriting and servicing. Gradient Labs runs its own Lending Agent across the borrower lifecycle, while the two specialists below focus on the front of the journey: origination.

9. Casca: best for AI-native loan origination

Casca (built by Cascading AI) runs an AI-native loan origination system used by FDIC-insured banks and fintechs, with a strong line in small-business and SBA lending. It raised a $29M Series A led by Canapi Ventures ($33M total), with customers including Live Oak Bank, Huntington National Bank, and Bankwell Bank.

Best for: banks and lenders modernising business and SBA loan origination.

10. Parlay: best for widening the lending funnel

Parlay runs a loan-readiness agent that pre-qualifies and packages applications, with an SBA focus, so more applications reach a decision rather than stalling at the top of the funnel. The seed-stage company, backed by JAM FINTOP, works with community banks and credit unions to lift SBA loan volume.

Best for: lenders that want to widen the top of the funnel without adding headcount.

How these agents fit together in a bank

The ten split into three jobs, and the split is the most useful thing to understand before you choose. Financial-crime and risk agents (Bretton AI, Sardine, Unit21, Hawk, Lucinity, Norm Ai, Oscilar) watch the money and the customer for risk. Lending agents (Casca, Parlay) move an application towards a decision. Gradient Labs runs the customer service AI around both: the conversations customers have, and the back-office cases like disputes, collections, and KYC that those conversations trigger.

Most banking work crosses these lines. A flagged transaction becomes a customer conversation. A loan in arrears becomes a collections case. A KYC review becomes a back-and-forth with the customer for documents. The financial-crime and lending agents do the specialist decisioning, and Gradient Labs runs the customer-facing operation that wraps around it. For the wider picture, see our AI in banking use case guide.

Which secure AI agent should your bank choose?

You need to run frontline and back-office customer operations under FS-native guardrails and US, UK, and EU coverage: Gradient Labs is the standout.

You want to automate financial-crime investigations: Bretton AI, Sardine, or Unit21, depending on whether you want investigations, a single fraud-and-AML platform, or detection-to-investigation in one loop.

You need transaction monitoring you can explain to a regulator: Hawk.

You want to speed up analysts without removing them: Lucinity.

You want regulation turned into automated checks: Norm Ai, or Oscilar for one layer across fraud, compliance, and credit.

You want to modernise lending: Casca for origination, Parlay for the top of the funnel.

If your bank's customer operations run end to end and compliance is non-negotiable, book a demo with Gradient Labs to see the agent on your own use case.