Choosing AI agents for lending means matching the right agent to the right job. A lending operation runs across origination, underwriting, servicing, and collections, and each stage has agents built for it. Some sit in the back end, scoring credit or reading documents. Others run the borrower conversations: the collections call, the hardship assessment, the application chase. The bar is highest when a vulnerable borrower or a regulated disclosure is on the line, which is why the EU AI Act classifies credit scoring and creditworthiness checks as high-risk. This guide ranks the best AI agents for lending across the jobs where AI now runs a lending operation: customer operations, loan origination, and credit decisioning.

Who is the best AI agent for lending in 2026?

Gradient Labs is the standout for lenders that need an AI agent across customer operations, because it runs the borrower conversations and the back-office case work on one platform, with guardrails on every turn and coverage across US, UK, and EU regulation. It covers the full borrower lifecycle: application support, onboarding, servicing, hardship, and collections, where point-solution agents handle a single stage.

Around it sits a strong field of specialist AI agent companies, each owning a different job in the lending stack: Casca and Parlay for loan origination, Taktile, Zest AI, and Scienaptic for credit decisioning, and Ocrolus for document processing. Most lenders will run more than one, so the useful question is not which single agent wins, but which one owns each job.

Platform | What it does | Where it fits in the lending stack | Best for |

|---|---|---|---|

Gradient Labs | Borrower conversations and back-office case work: collections, servicing, hardship, onboarding, application support | The customer-facing layer and the case work behind it | Lenders running collections, servicing, and support on one platform |

Casca | AI-native loan origination for business and SBA lending | Origination front office | Modernising business and SBA loan origination |

Parlay | Loan-readiness agent that pre-qualifies and packages applications | Origination top of funnel | Widening the lending funnel |

Taktile | Agentic credit and risk decisioning flows | The decisioning layer | Automating credit decisions across markets |

Zest AI | Machine-learning credit underwriting models | Underwriting | Banks and credit unions modernising underwriting |

Scienaptic | AI credit-decisioning platform | Underwriting and decisioning | Credit unions automating lending decisions |

Ocrolus | AI document and income analysis | Document processing in origination | Automating document and income verification |

What makes a good AI agent for lending?

A good AI agent for lending earns its place in one job and proves it can run that job safely. Use these five criteria to evaluate any vendor, and see our guide to how to choose an AI agent vendor for financial services for more depth.

Coverage of the borrower lifecycle, not just one stage: application, onboarding, servicing, hardship, and collections connect. An agent that handles one stage in isolation hands the borrower across a gap to the next tool or a human.

Regulatory coverage across your markets: US rules (FDCPA, TCPA, Reg F, UDAAP), UK rules (FCA Consumer Duty, CONC, Breathing Space), and EU rules (GDPR, EU AI Act) differ. An agent built around one market cannot safely run another.

Guardrails and human handoff on every turn: the agent should detect vulnerability, financial difficulty, and complaints in the moment, and hand the conversation to a human where regulation demands it.

A full audit trail: every decision, disclosure, and consent logged and timestamped, so the work survives a risk or compliance review.

Curing accounts, not just dialling: a strong collections agent secures a promise to pay and brings the account back to current, rather than logging a contact attempt and leaving the work on a human's desk.

Customer operations: the agent that runs the borrower conversation and the case

1. Gradient Labs: best for the end-to-end borrower lifecycle

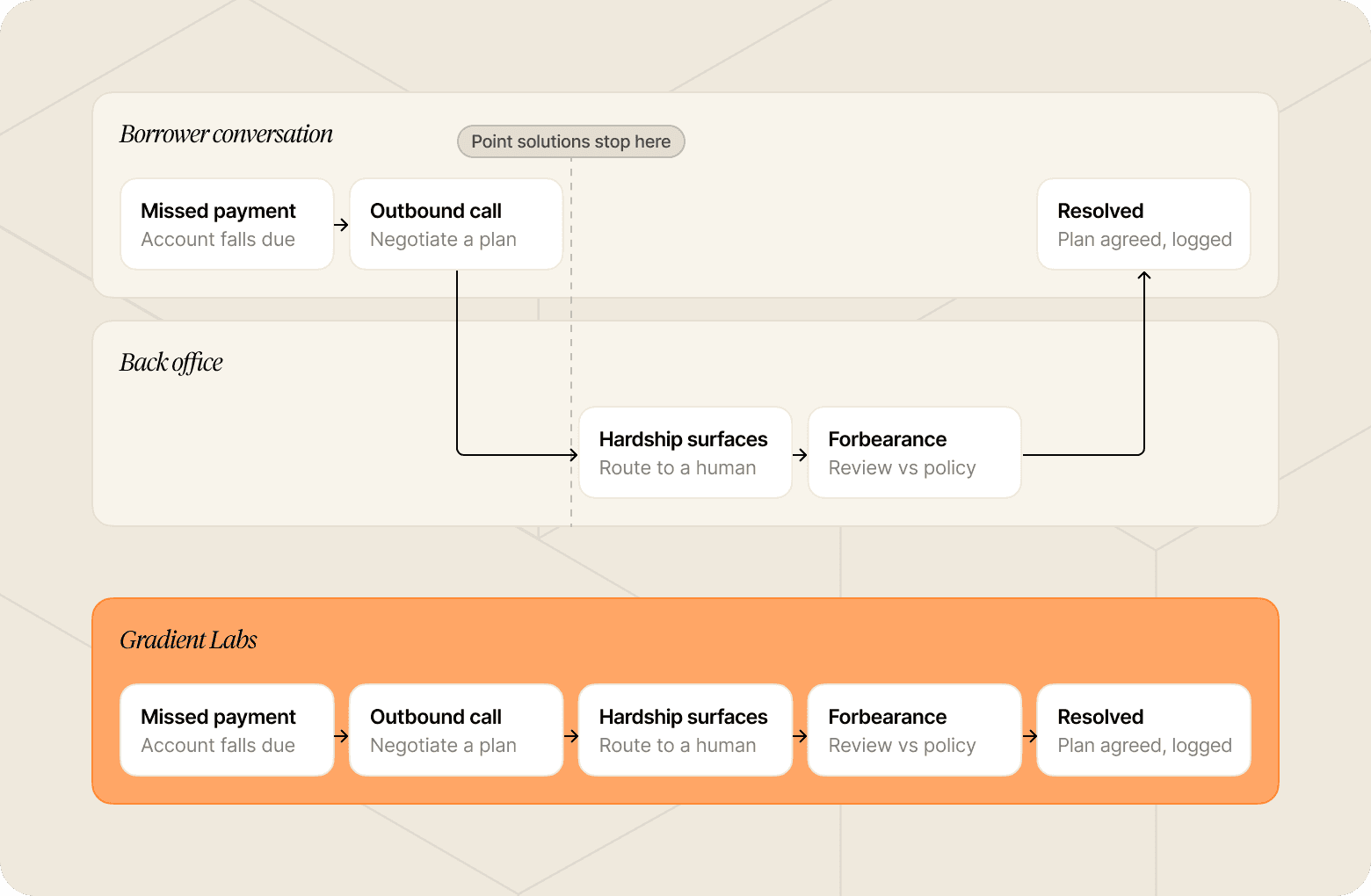

Gradient Labs is the AI-native customer operations platform for financial services, running both the borrower conversations and the back-office case work behind them on one platform. On the borrower-facing side that means conversational AI and customer support automation, not a chatbot bolted onto a single stage.

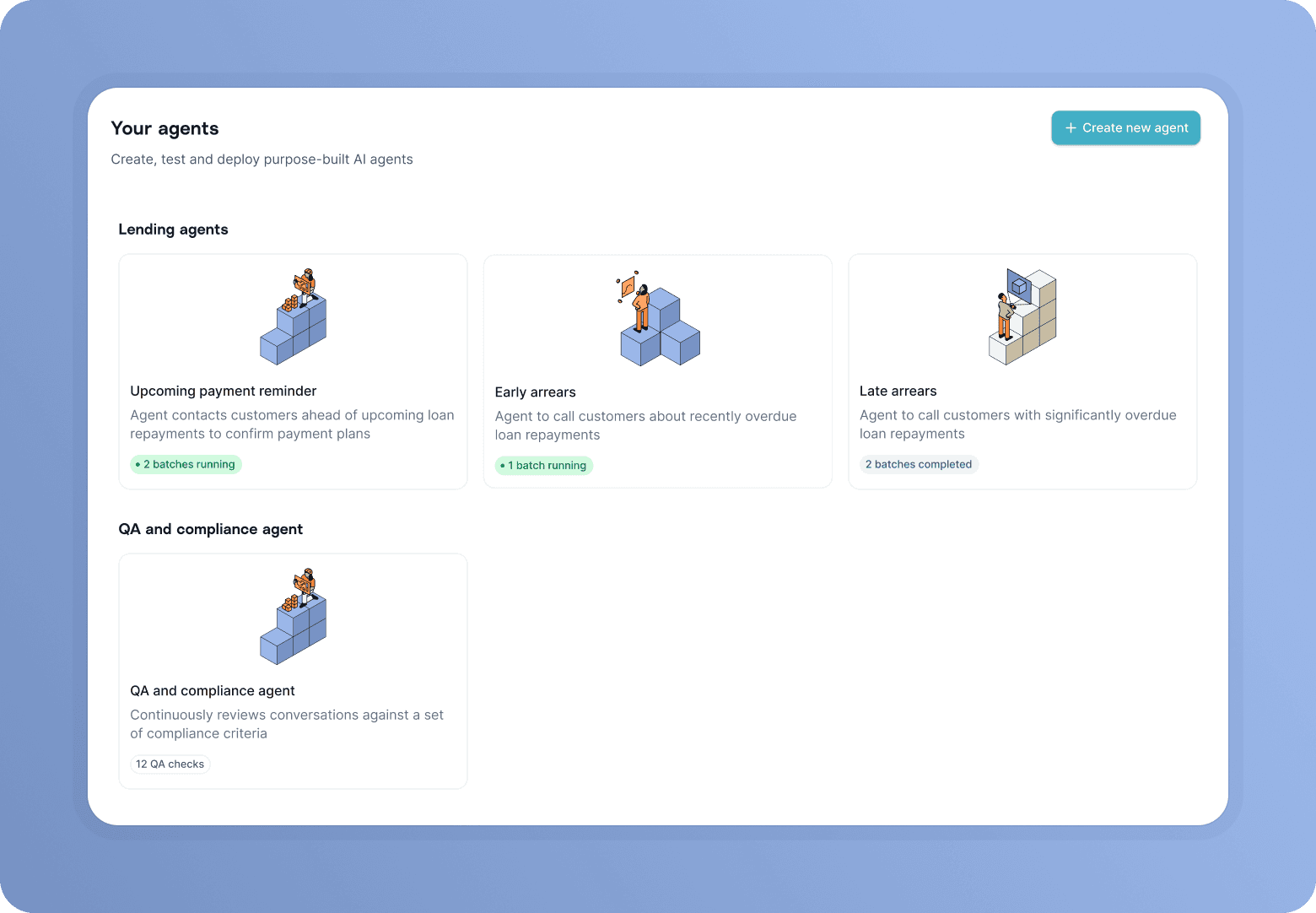

It covers the borrower lifecycle end to end: re-engaging application abandoners, onboarding new borrowers onto their repayment schedule, supporting active borrowers on balances and payment dates, running outbound collections, and handling hardship and forbearance.

In lending, a missed payment often becomes a collections call, the call surfaces hardship, and the hardship triggers a back-office review against the lender's forbearance policies. Where Gradient Labs runs that case end to end, point-solution collections bots stop at the call. Gradient Labs’ AI agent works across consumer lenders, BNPL providers, debt collectors, neobanks with a lending book, and community lenders.

Security and compliance: 20+ pre-built financial-services guardrails run on every turn, detecting vulnerability, financial difficulty, and complaints and handing off to a human where regulation demands it. Coverage spans US (FDCPA, TCPA, Reg F, UDAAP), UK (FCA Consumer Duty, CONC, Breathing Space), and EU (GDPR, EU AI Act) regulation. SOC 2 Type II is certified, data is encrypted at AES-256, and there are zero-day retention agreements with every LLM sub-processor.

Deployment: the finserv-native AI delivery team runs the migration from whatever you run today, so a non-technical ops lead can own the agent without staffing an AI team. Outbound collections can go live in a day on a CSV alone, with no integration required.

Recovery: a 1:1 recovery rate matching human collectors, 30x more compliant than human agents, and a 20% lift in cold customers reactivated within a month. Resolution climbs from 60% on day one to 80-90% in mature deployments as the team supercharges the agent in production.

Honest limitation: Gradient Labs runs the borrower conversations and the case work, not the credit decision. It does not score creditworthiness or underwrite a loan, so it sits alongside the decisioning and origination agents below rather than replacing them.

Best for: lenders running collections, servicing, and borrower support where compliance is non-negotiable. See the Lending Agent and overdue payment collections for the named work.

"Now we make 33,000 calls a month, converting 60% of engaged customers to committed repayment dates, all within FCA compliance standards. It has fundamentally changed how we manage the collections layer of our lending infrastructure."

— Violeta Filip, Head of Customer Experience, SteadyPay

Loan origination agents

Origination moves an application from interest to funding: answering eligibility questions, chasing documents, and packaging the file for a decision. The two specialists below automate the origination workflow itself. Gradient Labs supports the same stage from the borrower's side, re-engaging applicants who started but did not finish, while Casca and Parlay build and package the loan file.

2. Casca: best for AI-native loan origination

Casca (built by Cascading AI) runs an AI-native loan origination system used by FDIC-insured banks and fintechs, with a strong line in small-business and SBA lending. It raised a $29M Series A led by Canapi Ventures ($33M total), with customers including Live Oak Bank, Huntington National Bank, and Bankwell Bank. It is SOC 2 certified and holds borrower data in the US.

Best for: banks and lenders modernising business and SBA loan origination.

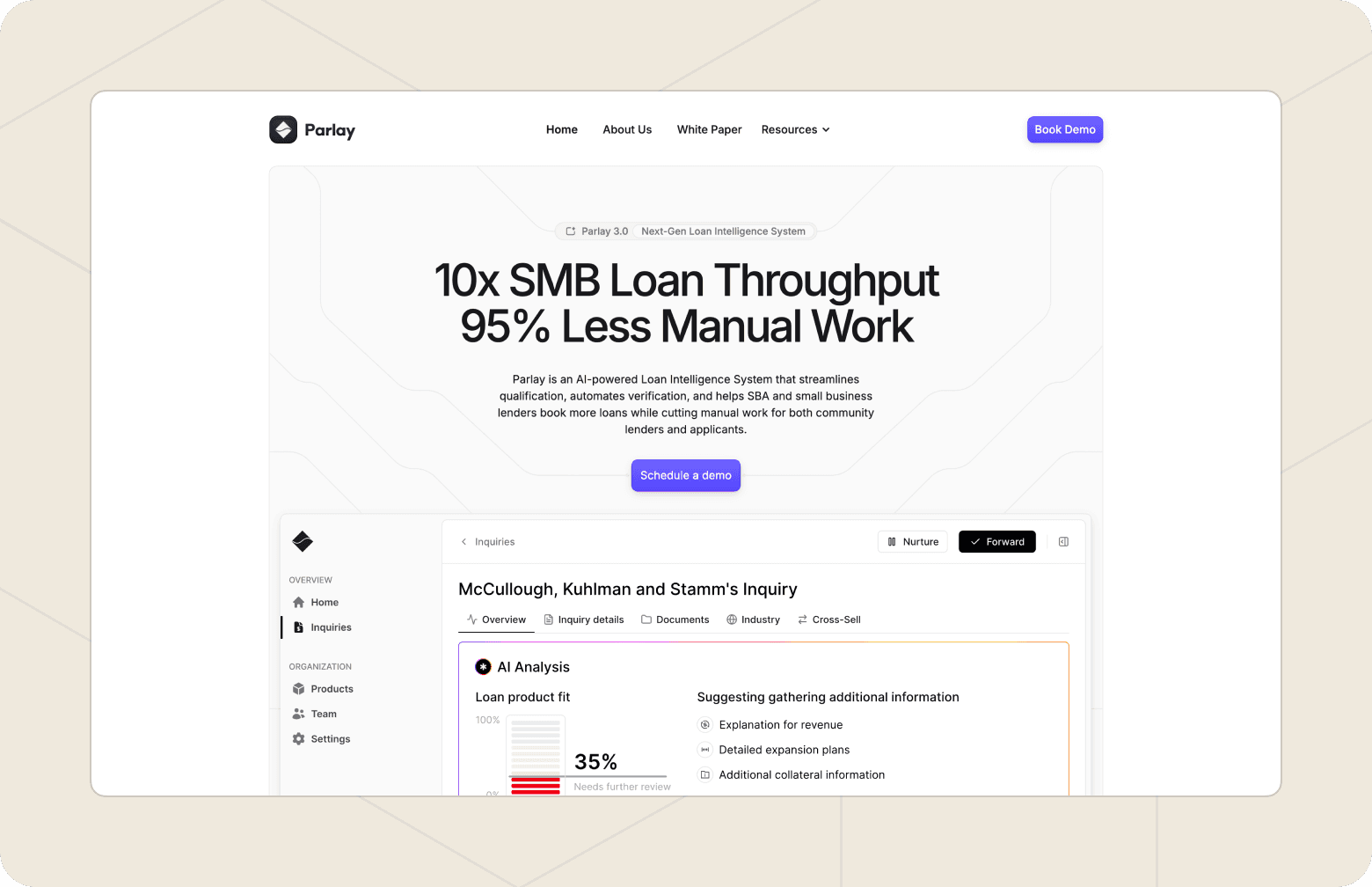

3. Parlay: best for widening the lending funnel

Parlay runs a loan-intelligence layer that pre-qualifies and packages applications before they reach a decision, so more applicants get to funding rather than stalling at the top of the funnel. The SBA-focused company raised a $2M seed led by JAM FINTOP and works with community lenders including First Internet Bank and Locality Bank.

Best for: community lenders widening the top of the funnel without adding headcount.

Credit decisioning and underwriting agents

Decisioning is the regulated heart of lending, where a model decides who gets credit and on what terms. Explainability and fair-lending controls matter here because every declined application has to survive a regulator's question about why it was declined. These three automate the decision while keeping it auditable.

4. Taktile: best for agentic credit decisioning

Taktile runs a no-code decisioning platform where risk teams build and deploy automated credit, fraud, and onboarding decision flows without engineering support. It raised a $54M Series B led by Balderton ($79M total) and runs across 24 markets, with customers including Mercury, Zilch, Allianz, and Rakuten Bank. Its global footprint suits multi-market lenders that need one decisioning layer across regions.

Best for: lenders automating credit decisions across multiple markets.

5. Zest AI: best for machine-learning underwriting

Zest AI builds custom machine-learning underwriting models for banks and credit unions, with a long-standing focus on explainability and fair-lending compliance. Founded in 2009, it works with around 300 lenders including SchoolsFirst and Members 1st credit unions, and closed a customer-led funding round in 2025. The fair-lending focus suits US lenders that need a defensible model behind every decision.

Best for: banks and credit unions modernising underwriting with explainable models.

6. Scienaptic: best for credit-union decisioning

Scienaptic runs an AI credit-decisioning platform delivered through a CUSO model built for credit unions, used by 150+ lenders including Genisys Credit Union. It packages decisioning for member-focused lenders that want to automate approvals without building the models in-house.

Best for: credit unions automating lending decisions at the member level.

Document processing

Lending runs on documents: pay stubs, bank statements, tax returns, and the income picture they add up to. Reading them by hand is slow and error-prone, and it sits in front of every credit decision.

7. Ocrolus: best for document and income analysis

Ocrolus automates document analysis and income and cash-flow assessment for lenders, turning raw borrower paperwork into structured data a decision can run on. It raised an $80M Series C and works with 400+ clients including Enova, PayPal, Brex, and SoFi. It sits in front of underwriting, so a decisioning model or a human reviewer gets clean inputs rather than scanned PDFs.

Best for: lenders automating document and income verification at the top of underwriting.

How these agents fit together across a lender's stack

The seven split across four jobs, and the split is the most useful thing to understand before you choose. Origination agents (Casca, Parlay) move an application towards a decision. Decisioning agents (Taktile, Zest AI, Scienaptic) make the credit call and keep it auditable. Ocrolus reads the documents that feed that call. Gradient Labs runs the customer operation around all of it: the conversations a borrower has across their loan, and the back-office cases like collections and hardship that those conversations trigger.

Most lending work crosses these lines. An abandoned application becomes an outbound nudge. A funded loan becomes an onboarding call. A missed payment becomes a collections case, and that call surfaces hardship that routes to a human. The origination and decisioning agents do the specialist work at each stage, and Gradient Labs runs the borrower-facing operation that wraps around it. For the wider picture, see our guide to deploying AI agents in lending, and for the equivalent landscape across a whole bank, the best secure AI agents for banking.

Which AI agent should your lending business choose?

You need to run collections, servicing, and borrower support under FS-native guardrails and US, UK, and EU coverage: Gradient Labs is the standout.

You want to modernise loan origination: Casca for business and SBA origination, Parlay for widening the top of the funnel.

You need to automate the credit decision: Taktile for multi-market decisioning, Zest AI for explainable underwriting, or Scienaptic for credit-union lending.

You want to automate document and income review: Ocrolus.

If your lending operation runs across the borrower lifecycle and compliance is non-negotiable, book a demo with Gradient Labs to see the agent on your own use case.

Elizabeth Shew leads Brand and Advocacy at Gradient Labs, where AI agents handle customer support and back-office work for banks, lenders, and fintechs. Before that, she led customer marketing at Mastercard and built Dynamic Yield's customer marketing programme from the ground up, a decade spent turning customer results into industry-shaping stories. She writes about how support and operations teams actually put AI and technology to work. Before tech, she was a professional dancer in NYC.