When a customer is stuck at a foreign checkout and their card doesn't work, a bank's reputation is on the line. What happens next, either fast help or none at all, is how your customer will remember you. It is one of the most consequential moments in the bank/customer relationship, yet the data shows most banks are failing to meet expectations. Gradient Labs surveyed 1,998 travellers about banking and payment problems abroad to better understand how AI agents can help close the gap.

These failures are common, and they cluster at the worst possible moments. Cross-border transactions, unfamiliar networks, and fraud detection calibrated for spending at home have gaps that customers typically encounter when the stakes are high and there's no fallback: a payment frozen mid-trip, a card blocked in a different time zone, with no one reachable to fix it. Half of the travellers we surveyed (1,000 of them) report experiencing a card, payment, or banking issue while abroad in the past two years.

Almost all of it is solvable now. A capable AI agent can answer at any hour, in any language, diagnose the problem, reassure the customer, and resolve it end to end or escalate cleanly when a human is needed. The banks that invest in AI agents cut support costs and earn loyalty that lasts long after a customer's trip, at the exact moment most competitors lose it. The analysis that follows focuses on these affected travellers: what the failures cost them, and where the opportunity lies.

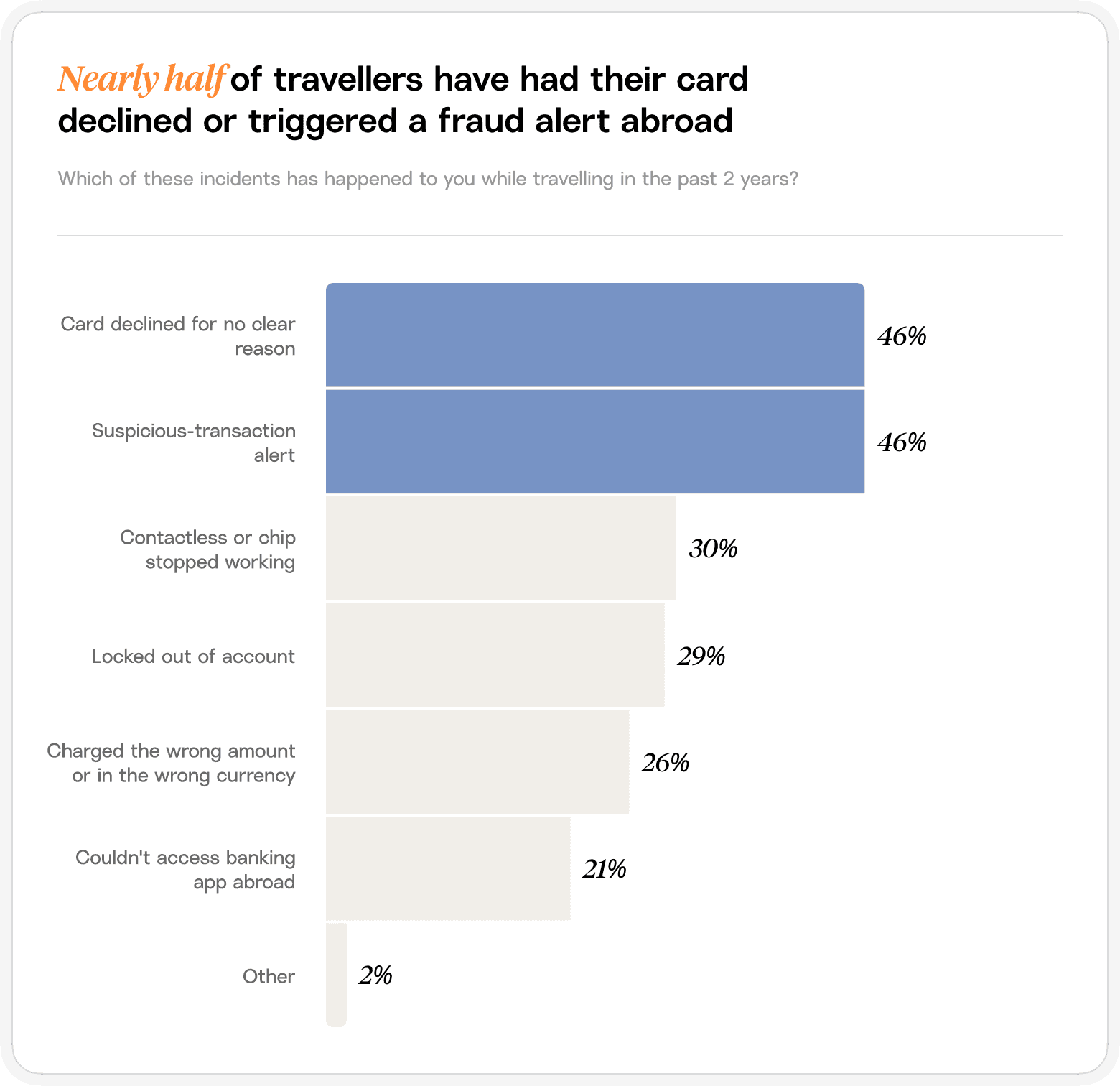

Most travellers experience banking problems abroad

Card declines and fraud alerts are the two most common incidents, each affecting nearly half of the affected travellers surveyed. They are the recurring, predictable reality of international travel banking. The 46% experiencing card declines and the 46% hit by fraud alerts are not two different populations; many are the same traveller, affected more than once, on more than one trip.

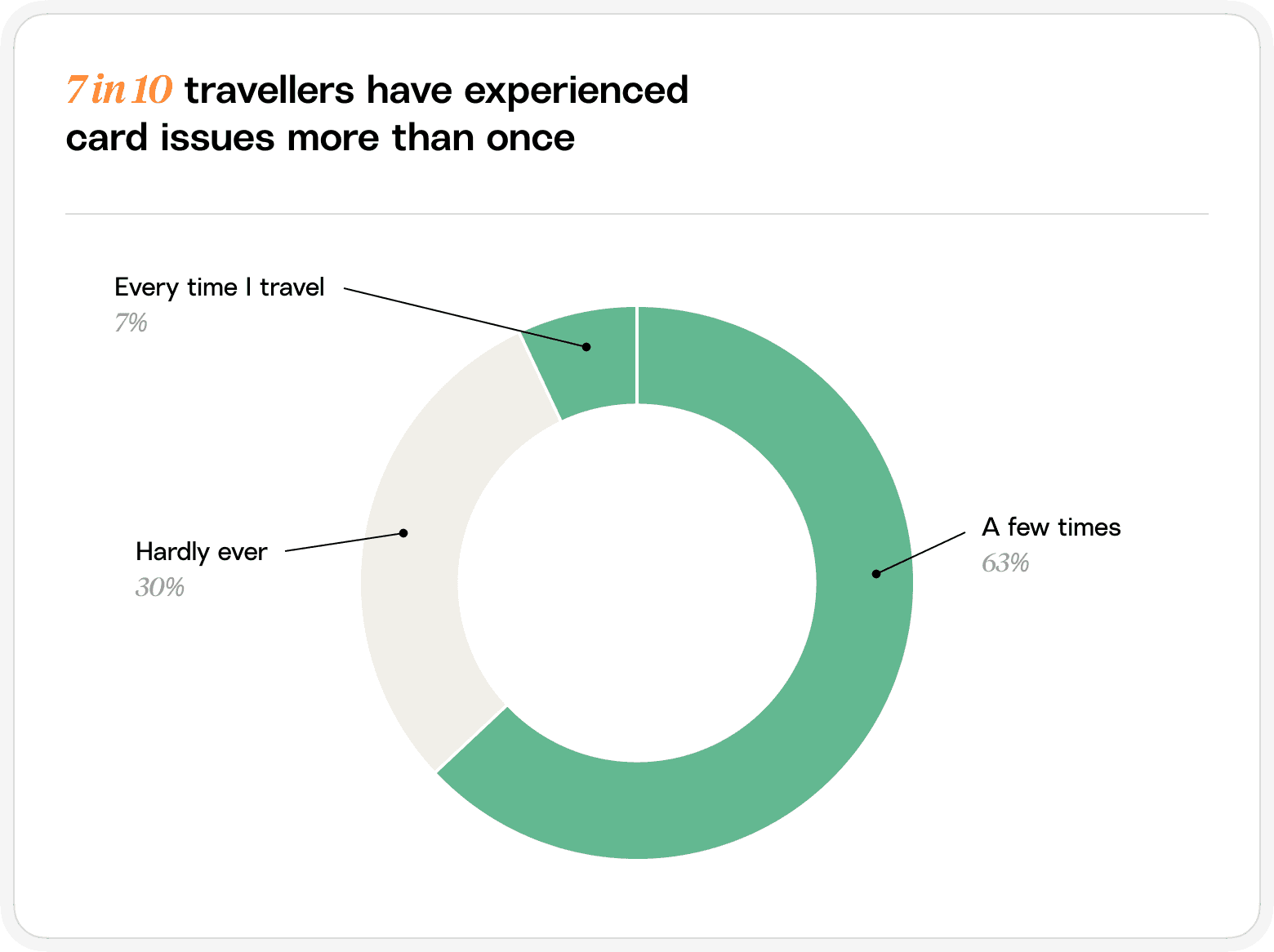

The 7% who say problems occur every time they travel represent a cohort that has normalised failure as part of their travel experience. Frequent travellers are disproportionately valuable to financial institutions, as they tend to spend more than infrequent travellers. The fact that this valued group is also disproportionately exposed to payment friction is a gap the industry has yet to fully close.

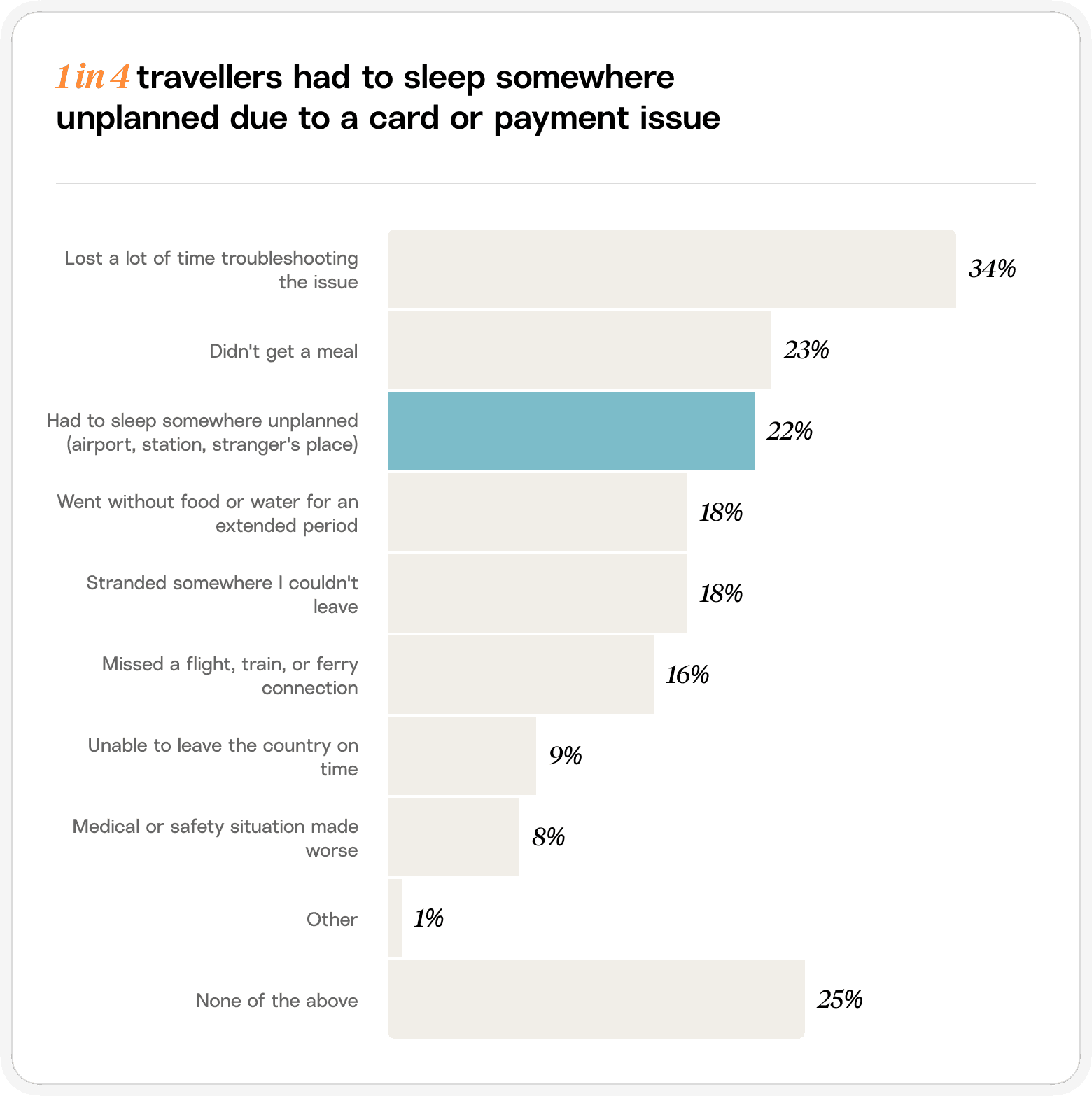

A third of affected travellers (34%) lost significant time troubleshooting. More than one in five (22%) had to sleep somewhere unplanned, and 18% were stranded somewhere they couldn't leave. These are high-stakes experiences with major inconveniences; these reframe how a person thinks about their bank and the card or account they'll use while travelling.

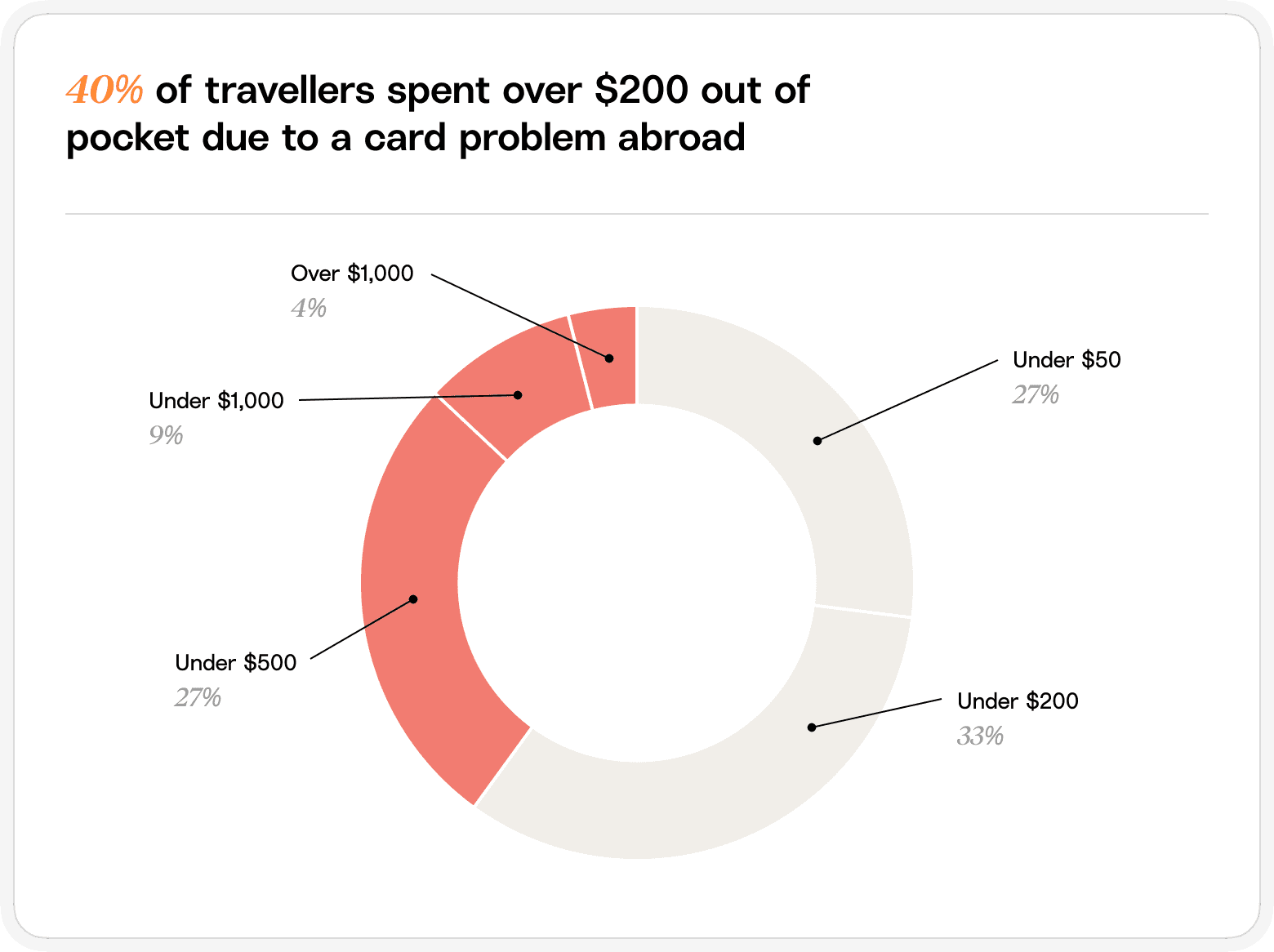

Banking problems abroad cause travellers to pay out of pocket

40% of affected travellers spent over $200 out of pocket as a direct result of a payment problem abroad, and 13% spent more than $500. These unplanned costs, which are the equivalent of an extra night in a hotel room or even a full day of travel, can undermine a person's travel budget and create a significant financial burden. The fact that they are entirely avoidable and purely the result of a bank's policies, processes, or availability can have a major impact on customer loyalty. While the cost to the customer is high in the short term, the cost to the bank is much higher in the long run.

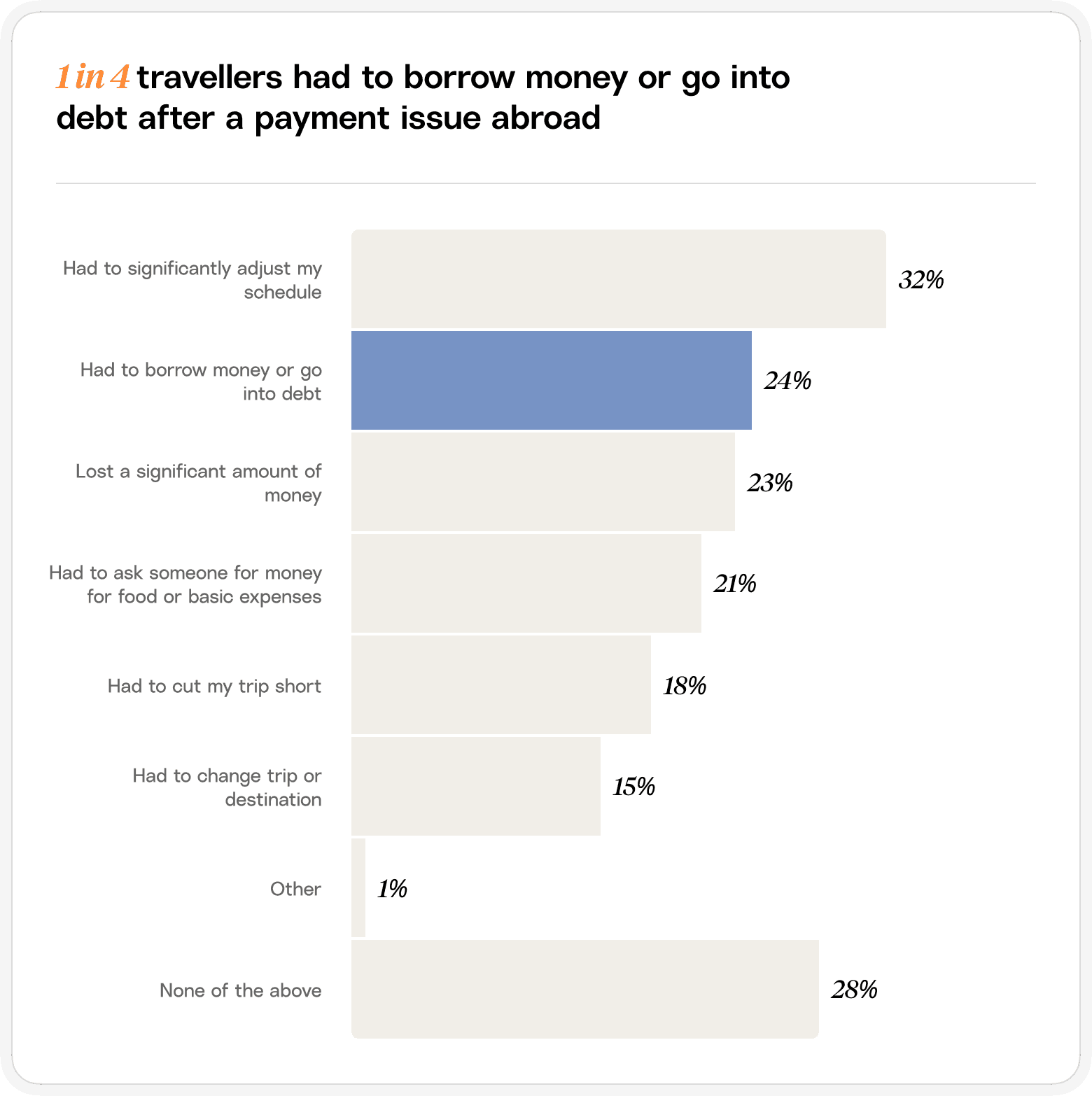

One in four travellers (24%) had to borrow money or go into debt due to a payment issue abroad. One in three (32%) had to significantly adjust their schedule. These are major disruptions that affect a customer's sense of financial security, happiness with their trip, and even their sense that their time, money, and PTO were well spent. These factors can overshadow a customer's original reasons for opening the bank account or card, such as immediate rewards, credit line, convenience, fair policies, etc. It can have a significant negative impact on customer loyalty and desire to recommend the bank to others.

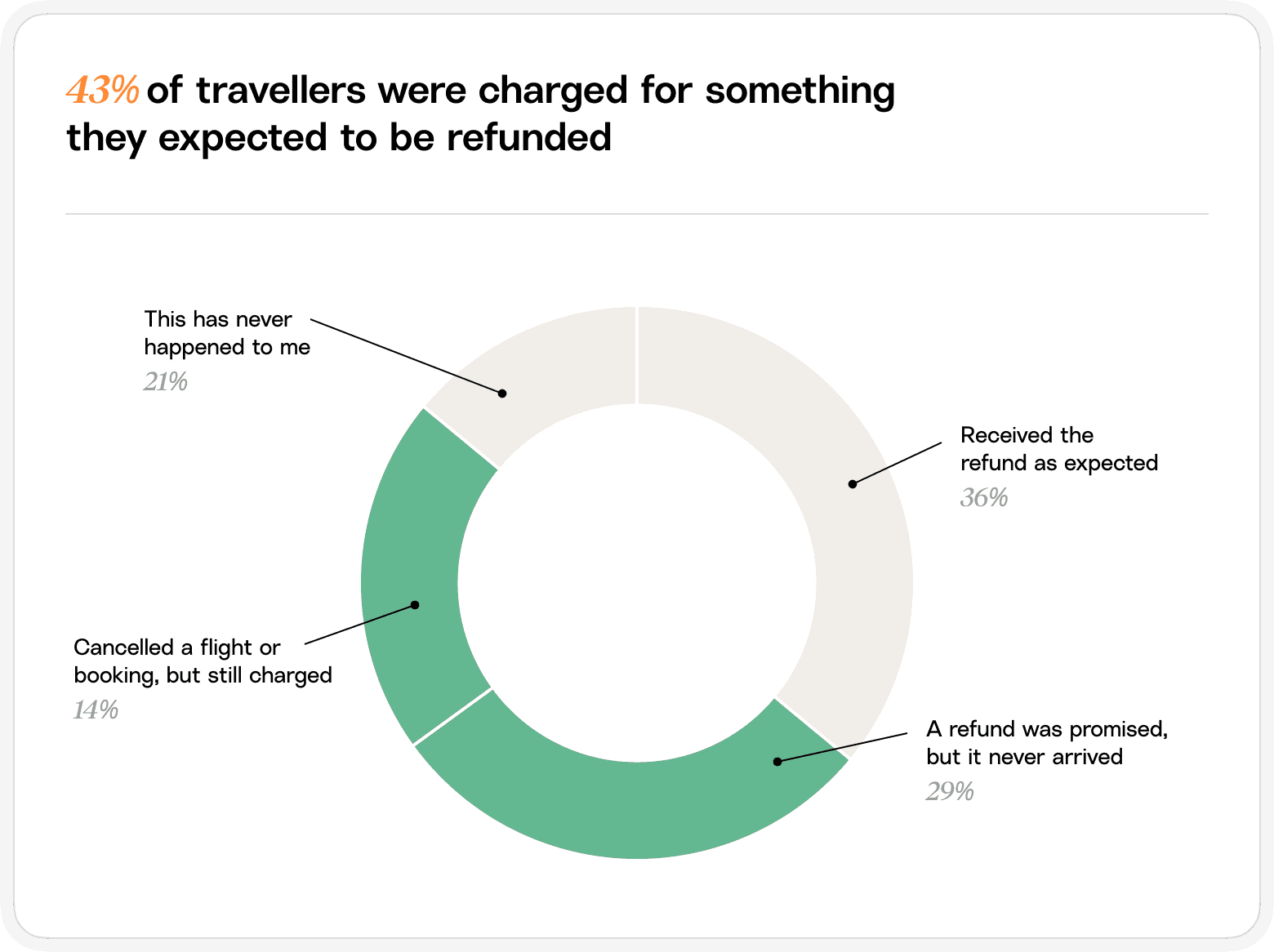

When plans change and a policy for reimbursement exists, travellers naturally expect certain unplanned costs to be covered by their bank or associated booking systems. But data reveals that most travellers never see reimbursement. Twenty-nine percent were promised one that never came, and 14% were charged outright for a cancelled booking. For customers, the gap between what they were told and what they received is the story they tell about their bank.

Travellers are frustrated by poor banking support

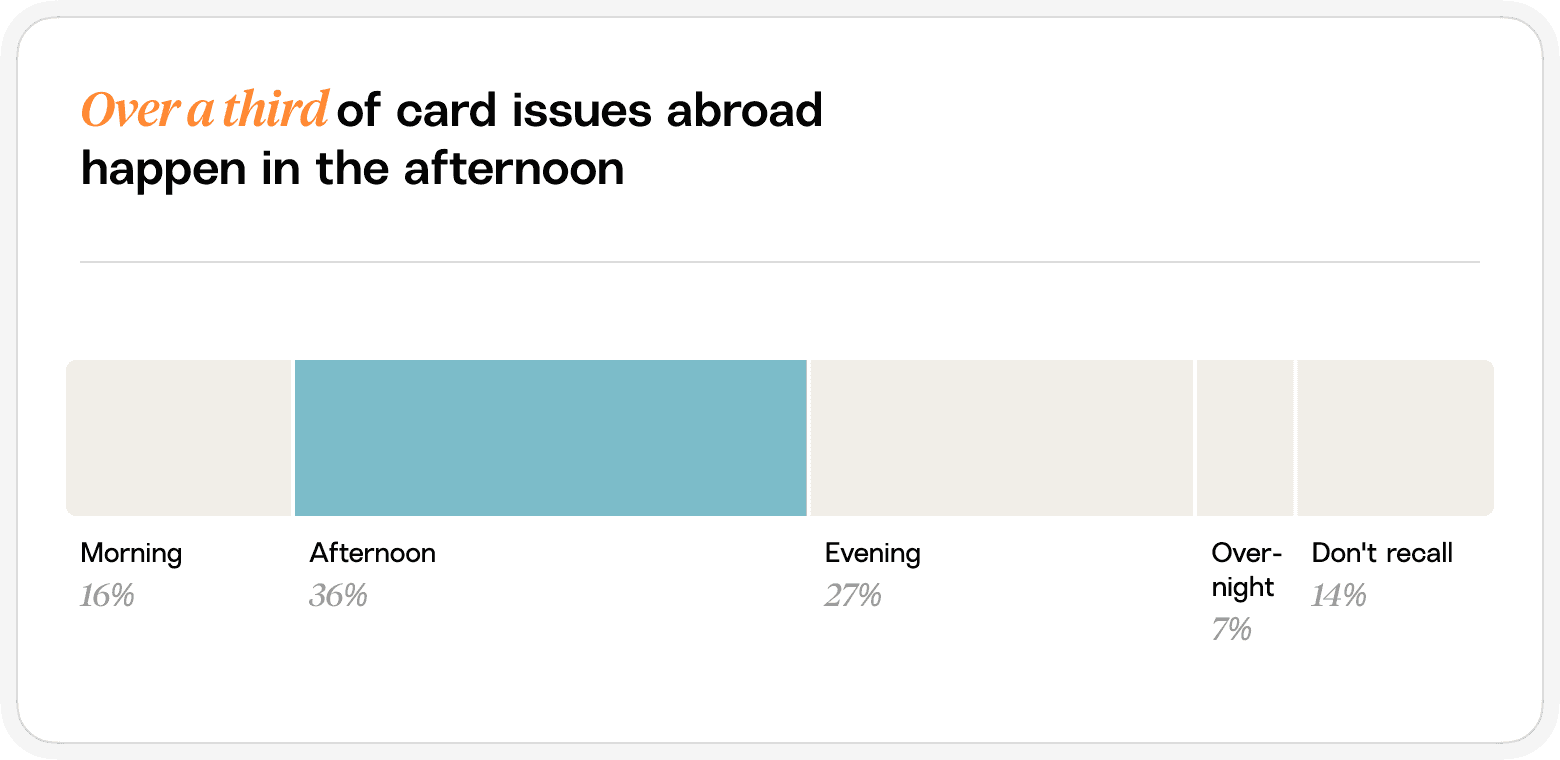

Over a third of incidents (36%) happen in the afternoon and 27% in the evening, but 7% occur overnight. Unlike domestic issues, a traveller in a foreign time zone may be contending with a problem that doesn't fall within business hours at home. A bank's availability is most sensitive in an emergency, and customers can feel abandoned if they have no options for getting in touch. Here, customer-facing AI agents have enormous potential to transform the traveller experience, as an AI agent can gather information, escalate tickets, provide reassurance, or even solve a problem outright at any hour of the day.

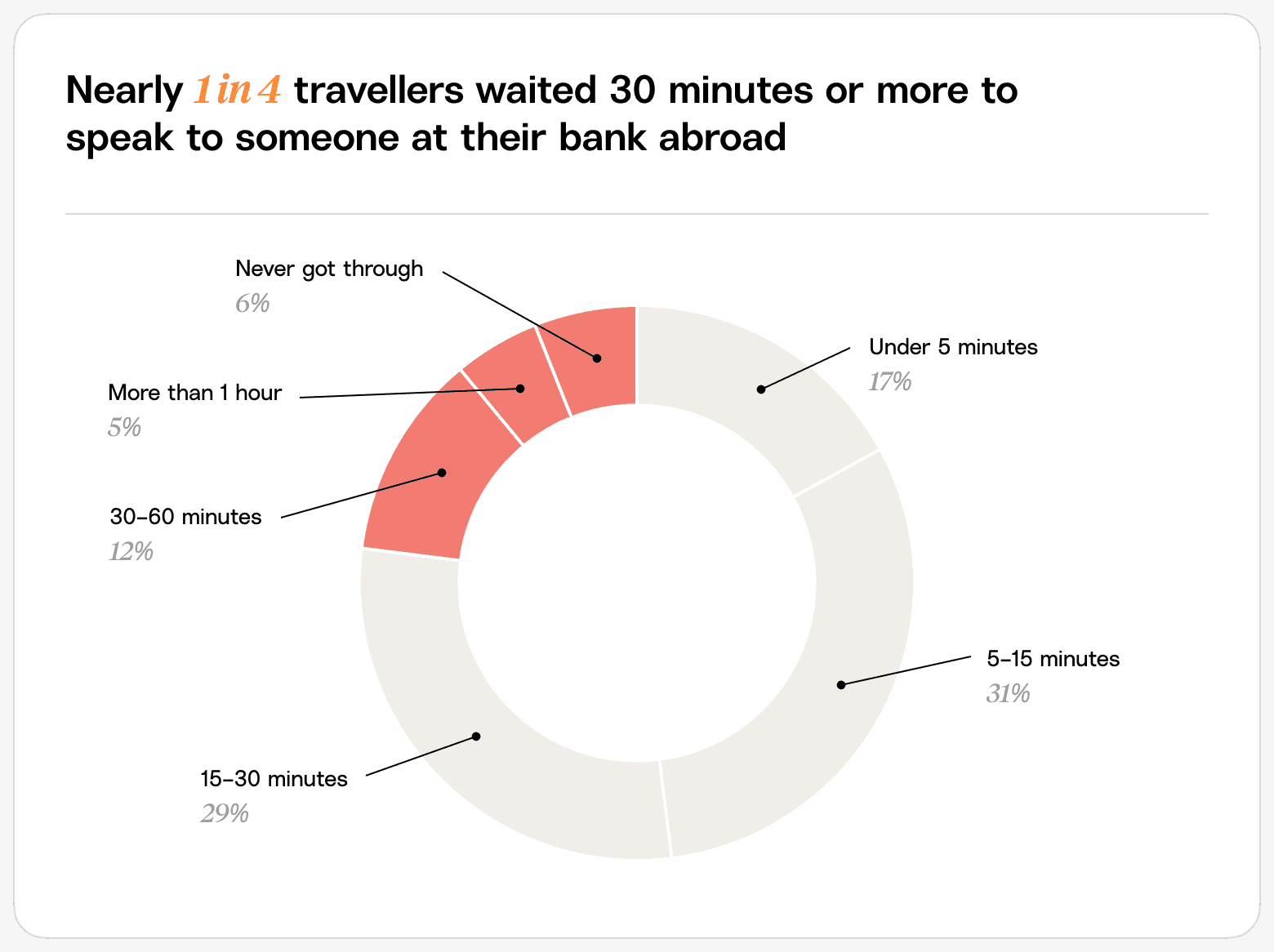

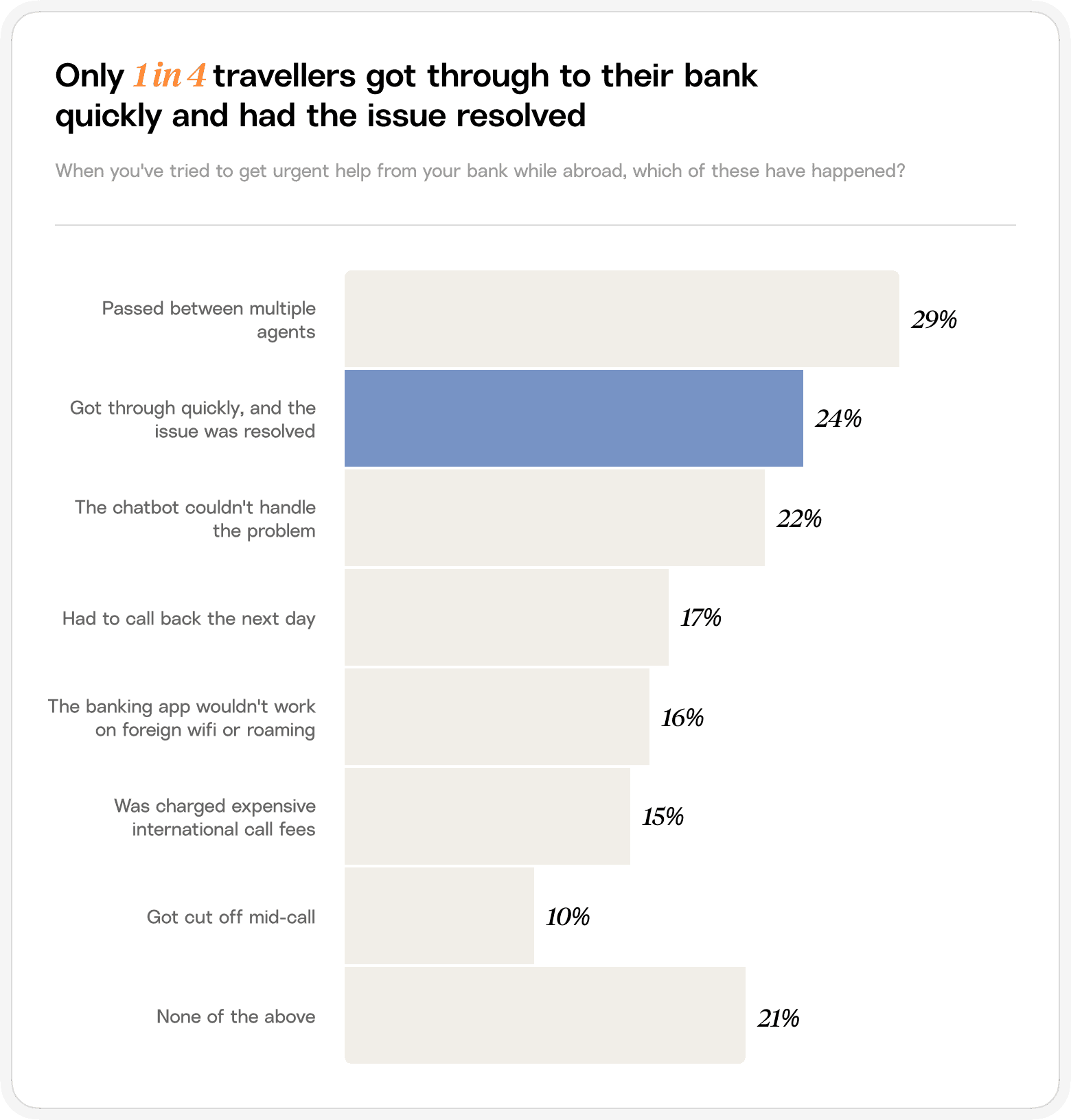

Nearly a quarter of travellers waited 30 minutes or more to speak to someone at their bank abroad. Six percent never got through at all. Every minute on hold in a foreign country is a minute the customer spends reconsidering their bank. It can also come with unexpected call costs and derail the traveller's plans for sightseeing, compounding an already-poor experience. Banks without reliable fallback systems for handling spikes in support demand risk their customer relationships and loyalty. Here, AI agents can also play a role by absorbing volume and low-lift cases, leaving human agents free to handle truly tricky cases that require judgment.

A customer who gets routed to an AI agent that can't resolve their issue, then transferred to a human who needs the full context re-explained, is unlikely to feel their time is being well spent. The 24% who got through quickly and had the issue resolved represent the benchmark. The question for the industry is how to make that the rule rather than the exception. The quality of the AI agent in this case plays a huge part, determined by CSAT benchmarks and how well it can integrate with back office systems and human hand-off (if needed). Getting the right AI vendor is critical for banks to reap the benefits of this technology and win on customer satisfaction.

A significant gap between customer expectations and the support they receive remains evident, with half of travellers describing their bank as somewhat helpful or not helpful at all. Consistently low scores amongst this contingent can have a long-term impact on a bank's overall CSAT rating, which is more significant when you consider that this demographic tends to spend more than the average customer.

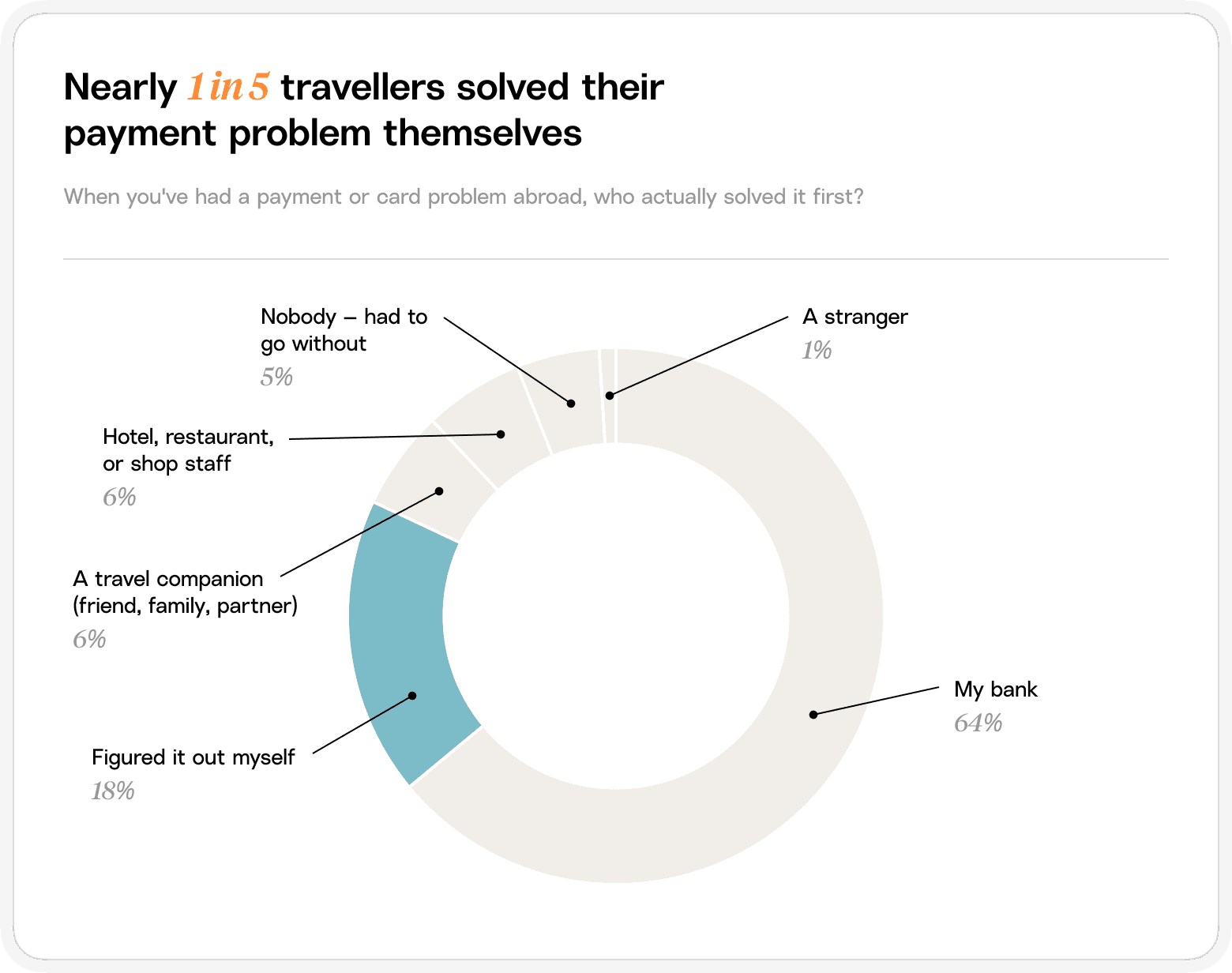

Many travellers hit dead ends with banks

18% of travellers end up solving the problem themselves, and 5% simply go without any resolution. That final number, one in twenty travellers experiencing a genuine dead end, is the one the industry should be most focused on.

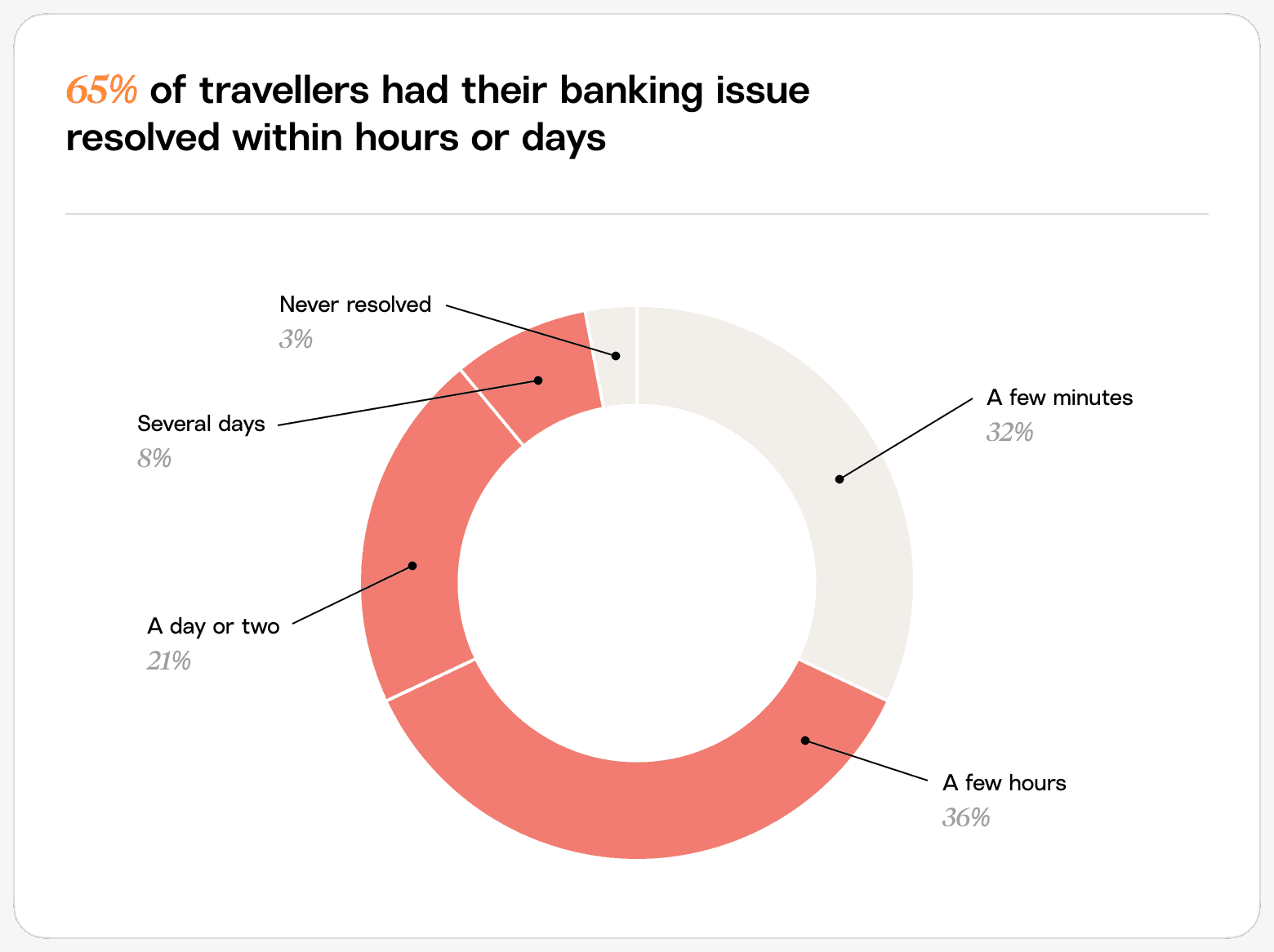

For customers whose issues do get resolved, how long does it take?

68% had their issue resolved within a few hours, 32% in a matter of minutes. That is proof that fast resolution is operationally achievable. The institutions already delivering in minutes for most customers have the infrastructure. The gap is consistency, something that suffers when a bank doesn't have contingencies for periods of high volume or cases that fall outside business hours.

Banking problems abroad risk customer loyalty

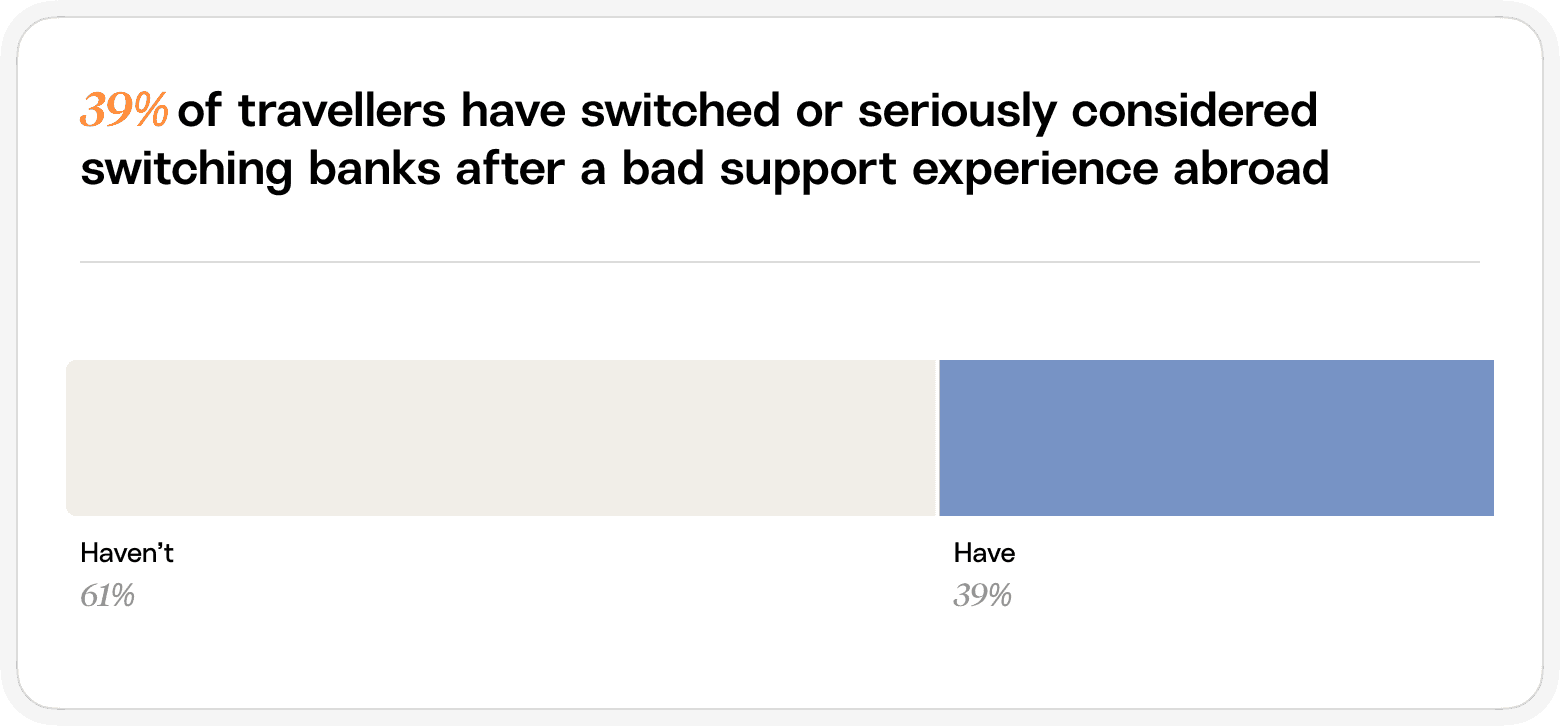

The ultimate measure of how the industry is performing is whether customers stay. 39% of travellers have switched or seriously considered switching banks after a bad support experience abroad. It is also, viewed differently, a market opportunity of the same size: 39% of customers are actively looking for a bank that does this better. The institutions building the infrastructure to deliver consistent, fast, human-quality resolution at any hour are the ones these four in ten travellers are waiting to find.

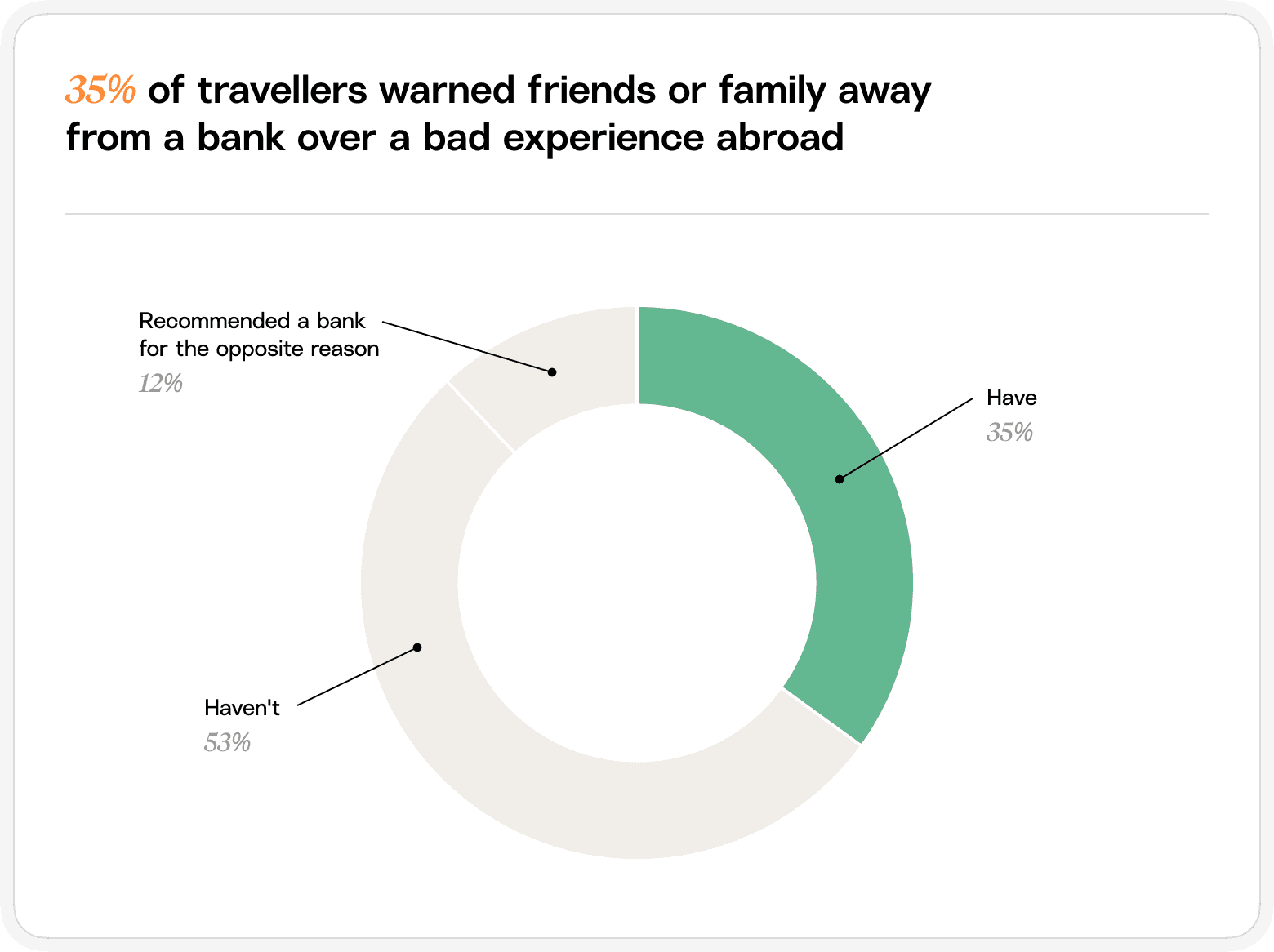

How a bank handles a problem abroad doesn't stay between the bank and the customer. 35% of travellers have actively warned friends or family away from a specific bank based on how it handled a problem abroad.

However, the inverse is equally powerful: 12% have recommended a bank specifically because it handled a problem well. Word-of-mouth in financial services is slow to build and fast to destroy.

Banks can close the support gap for travellers with AI agents

Three things stand out across the data. First, failure is common and expensive: half of travellers hit a problem abroad, 40% were left more than $200 out of pocket, and one in four had to borrow money or go into debt. Second, fast resolution is already achievable: a third of resolved cases close in minutes, so the benchmark exists and some banks are already meeting it; the challenge for these cases may be expanding availability, so these fast fixes can be achieved immediately, no matter the time zone. Third, loyalty is on the line: two in five travellers have switched or considered switching banks over a bad experience abroad, and the same share are waiting for a bank that handles it better.

Put together, these point to one conclusion. The banks meeting the benchmark don't have better technology than the rest. They have consistency: fast, human-quality resolution at any hour, in any time zone, even when volume spikes or a case falls outside business hours.

That consistency is exactly what a capable AI agent delivers. It answers the moment a customer is stranded, resolves the common problems outright, and hands the genuinely complex ones to a human with full context attached and plenty of reassurance for the customer.

Financial services is in the early stages of competing on support quality. The banks that close this gap will earn the loyalty the rest are giving away, at the precise moment it matters most. For a growing number of them, a capable AI agent is how they close it.

Methodology: Gradient Labs surveyed 1,998 travellers about their banking and payment experiences while travelling abroad. Among them, 1,000 reported experiencing a card, payment, or banking issue while abroad in the past two years. All findings in this report are based on responses from these affected travellers. Figures are based on self-reported responses. Percentages reflect the share of respondents selecting each answer; totals may exceed 100% for multi-select questions.

Gradient Labs builds AI agents that eliminate the manual work of customer operations. Their suite of specialist AI agents automate long-running processes in financial services, from lending and disputes to KYC. These agents work together across frontline support on voice, text, and email, back-office workflows, and all the operations in between. Founded by Monzo's former AI leadership and trusted by some of the biggest names in finance, including Wise, Current, and Zego, Gradient Labs is purpose-built for finance and the regulatory compliance it requires. Their AI agents outperform human teams on CSAT and QA scores and remain undefeated on resolution rate, driving widespread adoption across financial services, including some of the largest AI deployments in the industry.