Most lenders have already run an AI pilot. Far fewer have managed to deploy AI agents in lending that recover at the rate a good human collector does, stay compliant during outreach, and hold up when risk and compliance look under the bonnet. MIT's Project NANDA found that 95% of enterprise AI pilots deliver no measurable return, and in lending the gap rarely comes down to the model. It comes down to deployment: the internal buy-in, the guardrails, the integrations, and the ramp up, all of which turn a promising demo into a beneficial system that risk and compliance will sign off on.

This guide breaks down how to deploy AI agents in lending into six steps, in the order a collections and servicing operation actually works through them, so your first deployment cures accounts and your second one is easier. It is the lending companion to our guide on how to deploy AI agents in banking.

1. Choose the right AI agent for the borrower lifecycle

A generic AI agent answers a question and closes the conversation. It copes with "what's my balance?" or "when's my next payment due?" but plateaus around 60% automation on a real lending operation, because most of the manual work in lending doesn't fit the one question, one answer shape.

Collections is the clearest example. A borrower misses a payment, the account moves through pre-arrears into early arrears, and someone has to reach out at the right time on the right channel, verify identity, explain the balance, work through repayment options, agree on a plan, capture the promise to pay, update the servicing system, and follow up days later if the money doesn't land. Hardship, forbearance, and vulnerable customer handling run the same way: long processes against regulatory deadlines, not quick replies.

A specialist agent like the Gradient Labs Lending Agent is better for lenders on three fronts:

It runs the borrower lifecycle, not just the reply: application chase, onboarding, servicing, and collections each need intake, action, follow-up, and close. A specialist agent shares memory and context across every stage. A generic agent's case stops at the first response.

Compliance is built in: in lending, the wrong tone with a struggling borrower can be a regulatory breach, not just a poor experience. Lenders need agents that run finance-specific guardrails on every turn, with vulnerability detection, hardship signals, and no pressure selling, all on a full audit trail. Horizontal tools treat compliance as a configuration layer you build and maintain yourself.

It acts inside your systems: resolving an arrears case means reading the live balance, presenting eligible repayment options, taking the payment, and setting up the direct debit. A specialist agent connects to your servicing platform and dialler to do the work, not just explain it.

Be critical about the work you're automating. If it's first-line FAQ, most tools cope. If it's overdue payment collections, hardship assessment, and promise-to-pay work that actually moves recovery, you need an agent built for the process. See how the options compare in our ranking of the best AI agents for lending. That depth is what lifts recovery past the ceiling that stalls generic agents, toward 80–90% in mature deployments.

2. Treat internal buy-in as the first step to deploy AI agents in lending

In a regulated lender, the agent has to pass your own people before it ever reaches a borrower. Risk, compliance, information security, and collections operations each hold a veto, and procurement moves at its own pace. Treat the internal sell as the first deployment task, not a formality that follows it.

Three gates tend to decide it:

Security review: your information security team assesses data handling, retention, encryption, and sub-processors, with call recordings and payment data squarely in scope. Come with answers: SOC 2 and ISO 27001, GDPR with full DSAR handling, AES-256 at rest, and zero-day data retention agreements with every LLM sub-processor.

Compliance review: risk and compliance check the agent against the rules you live under, whether that's FCA Consumer Duty and CONC in the UK, the FDCPA and Regulation F in the US, or GDPR and the EU AI Act in Europe. The audit trail matters here as much as the model does.

Prioritisation: pick the first segment by impact, not by ease. Which delinquency stage and which book unlock the most recovery for the least integration? That answer sets the order of everything that follows.

Then scope the proof of concept around one concrete question the agent must answer: can it find the borrower, verify them, read the account status, present the right repayment options, and respond correctly under your guardrails?

Gradient Labs’ customer SteadyPay, an FCA-authorised embedded lending infrastructure company serving neobanks and fintech platforms, ran exactly this sequence: a security review and a tightly scoped collections pilot before a single live call. Gradient Labs guarantees the deployment once a use case is scoped. If we don't deliver what we agreed, you get your money back, which puts a floor under the decision for risk-averse stakeholders.

3. Teach the AI agent what your best collectors know

An AI agent knows what you give it, and a knowledge base on its own is never enough. Your best agents carry years of practised judgement that never made it into a document: how to reassure an applicant stalled on a document upload, how to walk a new borrower through their repayment schedule on a welcome call, how to read a customer who's struggling and know when to push for a plan and when to ease off, and the workaround for the account that doesn't fit the script. Getting that knowledge into the agent is one of the first steps in a deployment, and at Gradient Labs, three sources feed it:

Knowledge base: your policies and help articles, the documented baseline most teams already have.

Facts: the structured details that change often, like eligibility rules, fee schedules, repayment options, settlement figures, and cut-off times. These are kept separate because they're precise and they move.

Notes: your team's working knowledge, the judgement that never got written down. Gradient Labs generates it for you by analysing thousands of conversations your team has already handled, surfacing how your best people answer an eligibility question on an in-progress application, the tone they take with a vulnerable borrower in arrears, and the steps they take when a policy doesn't quite fit. Your team reviews what it surfaces, and it becomes guidance the agent applies from day one.

On top of knowledge sit procedures: your SOPs written as natural-language steps the agent executes, from application chase and onboarding to servicing and collections, with branching logic for the cases that don't follow the script.

Because the agent learns from your real conversation history rather than a blank slate, it starts near your team's standard instead of climbing there through months of escalations. Treat early gaps the way you would with a new hire: a poor response signals missing context, not a dead end.

4. Make sure your AI agent understands lending regulations

In most industries, a wrong answer from an AI agent means a poor customer experience. In lending, it can be a regulatory breach: unlicensed advice on which product to take, pressure on a vulnerable borrower in arrears, or a call placed outside permitted contact hours.

That raises the bar on what "working" means. The agent has to be controlled on every turn, and the controls have to be the platform's job, not a configuration layer your team builds and maintains.

At Gradient Labs, two kinds of guardrails do this work:

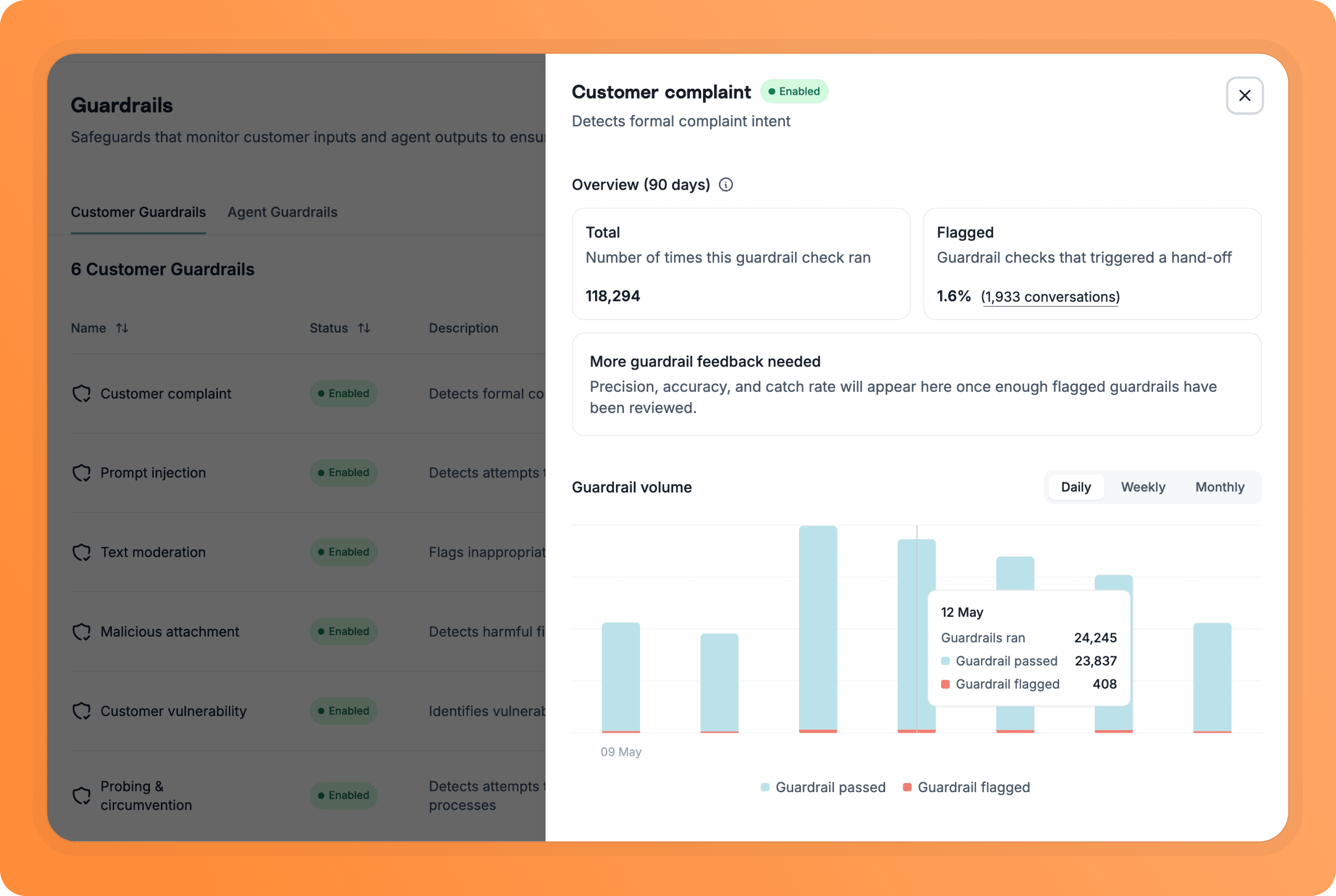

Customer guardrails read the conversation and act on it: detecting signs of financial difficulty or vulnerability that trigger consumer-protection obligations like FCA Consumer Duty, spotting a complaint, and handing off to a specialist when a human is needed.

Agent guardrails check what the agent is about to say or do: blocking unlicensed advice and pressure selling, holding to permitted contact windows, giving Mini-Miranda disclosures where US rules require them, and stopping sensitive data from leaving. They edit the draft before it reaches the borrower.

Gradient Labs runs 20+ pre-built financial services guardrails on every turn, with coverage across US (FDCPA, TCPA, Reg F, UDAAP), UK (FCA Consumer Duty, CONC, Breathing Space), and EU (GDPR, EU AI Act) rules. Every action, disclosure, consent, and decision lands in an audit trail your risk and compliance teams can review. The result is an agent that runs 30x more compliant than human agents, because the controls never have an off day.

5. Deploy AI agents in lending: start outbound in a day

Here is where lending deployment differs from most. You don't have to wait for integration to go live. The Lending Agent can start CSV-only outbound work in under a day, with no integration required: re-engaging applicants who stalled before funding, welcoming new borrowers and walking them through their repayment schedule, sending payment reminders before an account slips into arrears, and even chasing overdue balances to capture a promise to pay. For that one, simply upload a segment, and the agent calls, verifies identity, and runs the conversation. That gives you live results and a real dataset while the integration work runs in parallel.

Then integration is where the agent goes from talking to resolving. Answering a question and resolving a case are different jobs. The agent earns its return when it can do advanced work, such as reading a live balance, taking a payment, setting up a direct debit, updating a settlement figure, and writing the outcome back to the case. That means connecting it to your servicing platform, CRM, and dialler through custom API tools, not a sync with the help centre alone.

The same connections open up inbound work too: active-borrower servicing queries, in-progress application support, and hardship cases that trigger a back-office review against your forbearance policies.

Sequence the integrations the way you sequenced the use cases. Connect what unblocks your highest-volume work first, then widen. This is where the economics turn. Much of the cost saving in AI programmes arrives past 80% automation, and the climb from 60% to 80% is mostly integration depth: the agent can't cure the account, complete the application, or resolve the servicing query if it can't see the data and take the action.

6. Earn trust by starting with one segment, then ramp

With this many stakeholders in a lending deployment, it's better to earn trust in increments, and a gradual ramp is how you build it. Start narrow and lower-risk: a payment-reminder campaign before accounts slip into arrears, a welcome-call programme for newly funded loans, or a single delinquency stage on a low-ticket debt book that's currently unprofitable to chase by hand, with human QA on every call. Then widen as the numbers hold. Gradient Labs’ customer SteadyPay scaled this way to 33,000 AI voice calls a month, a 60% conversion rate among verified customers, and a 20% lift in cold customers reactivated within one month.

Going live is the start line, not the finish. A mature deployment reaches 80–90% resolution, but day one usually lands around 60%, and the gap closes through a maintenance loop you run after launch:

Watch the handoff rate: every handoff to a human is an account the agent didn't cure.

Diagnose the root cause: missing knowledge, a gap in a procedure, or a missing integration.

Fix the source, then test and monitor: update the knowledge, procedure, or tool, validate it, and watch the rate move.

From there, growth runs on two axes: breadth (more segments, channels, and languages) and depth (more of the lifecycle, from hardship assessment and forbearance to onboarding and servicing). Recovery and borrower experience climb together: the Lending Agent matches human collectors 1:1 on recovery while staying 30x more compliant.

Deployment is the hard part, and it's the part Gradient Labs is built to carry: a lending-native platform, a delivery team that knows collections, and a guarantee on every use case we scope. If you're choosing where to start, book a demo and we'll plan your first deployment with you.

Elizabeth Shew leads Brand and Advocacy at Gradient Labs, where AI agents handle customer support and back-office work for banks, lenders, and fintechs. Before that, she led customer marketing at Mastercard and built Dynamic Yield's customer marketing programme from the ground up, a decade spent turning customer results into industry-shaping stories. She writes about how support and operations teams actually put AI and technology to work. Before tech, she was a professional dancer in NYC.