Credit unions run lean. A team of four handling member services for 50,000 members cannot absorb the same operational friction as a Tier 1 bank with a contact centre of 400. But members chose their credit union precisely because it felt personal, and replicating that at scale - while staying on the right side of NCUA examination, BSA obligations, and FDCPA compliance - is the problem AI agents now solve. This guide ranks the best AI agents for credit unions in 2026, grouped by the three jobs credit unions hire them for: member operations, financial crime and risk, and lending.

Who is the best AI agent for credit unions in 2026?

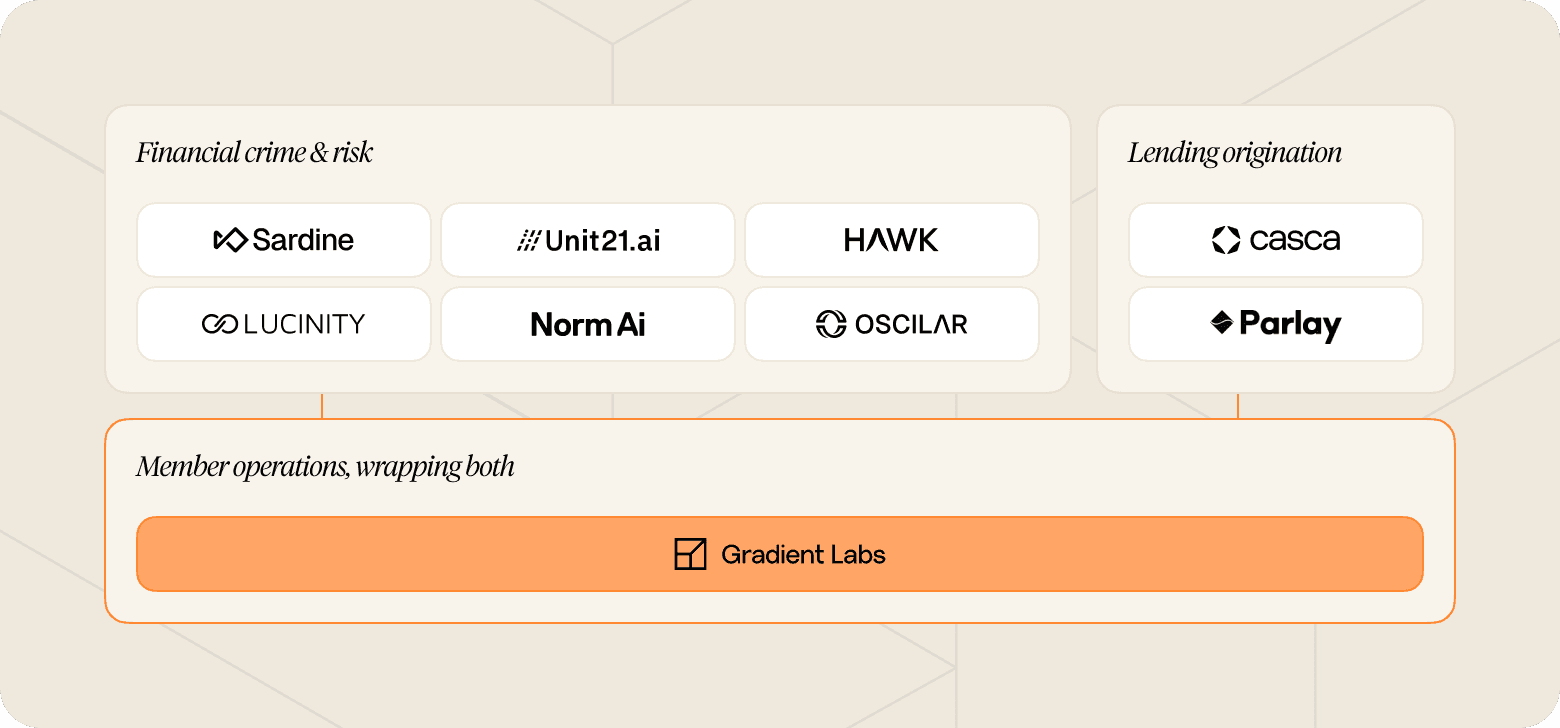

For member operations, Gradient Labs leads this ranking: one platform carries the frontline conversations and the back-office case work behind them, with FS-native guardrails on every turn and coverage across US regulation. The other eight agents own different jobs. Sardine, Unit21, Hawk, Lucinity, Norm Ai, and Oscilar cover financial crime and risk, while Casca and Parlay cover lending origination. A typical credit union will end up running several, which makes the real decision which agent owns each job, rather than which one tops the list.

Platform | What it does | Where it fits | Compliance posture | Best for |

|---|---|---|---|---|

Gradient Labs | Member-facing and back-office operations (disputes, collections, KYC) | The member-facing layer and the case work behind it | 20+ FS-native guardrails every turn, SOC 2 Type II, US/UK/EU coverage | Credit unions running member services and back-office work on one platform |

Sardine | Fraud, AML, and compliance on one risk platform | Fraud and FinCrime | FS-built risk platform | Fraud, AML, and compliance under one roof |

Unit21 | Agentic fraud and AML, detection through investigation | Fraud and AML operations | Human-readable audit trail, 2026 RegTech100 | Detection and case investigation in one loop |

Hawk | AML monitoring and sanctions screening on explainable AI | Transaction monitoring | Explainable AI, automated SAR drafting | Modernising transaction monitoring |

Lucinity | FinCrime investigation agents working alongside analysts | The FinCrime analyst desk | Human-in-control copilot model | Speeding up investigations without removing the analyst |

Norm Ai | Regulatory agents that encode laws and policy into checks | Compliance and legal | Regulation encoded into automated review | Turning regulatory requirements into automated checks |

Oscilar | AI agent hub across fraud, AML, credit risk, and onboarding | Risk-decisioning layer | Used across 100+ financial institutions | One risk layer across fraud, compliance, and credit |

Casca | AI-native loan origination for business and SBA lending | Lending front office | Used by FDIC-insured banks | Modernising loan origination |

Parlay | Loan-readiness agent that pre-qualifies and packages applications | Lending top of funnel | Works with community banks and credit unions | Widening the lending funnel |

What makes a good AI agent for a credit union?

Choosing an AI agent for a credit union is different from choosing one for a neobank or a Tier 1. The same holds for AI agents for community banks, which share the lean-team economics even though examination comes from the FDIC or OCC rather than the NCUA. Five criteria separate the vendors that can work in this environment from the rest; for more depth, see our guide to choosing an AI agent for financial services.

NCUA-compatible compliance posture: credit unions are examined by the NCUA, not the OCC. The agent has to produce audit-ready outputs, handle member data under BSA obligations, and treat vulnerable members in line with CFPB expectations. Ask every vendor directly how they support NCUA examination.

Guardrails on every turn: the agent should catch the risky moments before they reach a member, whether that is a complaint that needs escalating, a member showing signs of financial difficulty, or a collections call that risks stepping outside FDCPA boundaries.

A full audit trail: examiners scrutinise credit unions on the same workflows they scrutinise banks, so every action, tool call, and reasoning step needs a log entry that survives the review.

Data security your IT team can stand behind: treat SOC 2 Type II, encryption at rest and in transit, and zero-day data retention with every LLM sub-processor as entry requirements. Credit unions often run lean IT functions - the vendor's security posture has to carry the weight.

Deployment without an AI engineering team: a vendor that hands over an SDK and leaves is not built for a credit union ops team. Look for a provider whose delivery team runs the migration and whose product a non-technical ops lead can own day-to-day.

Member operations: one agent for the conversation and the case behind it

1. Gradient Labs: best for end-to-end credit union member operations

Gradient Labs is the AI-native customer operations platform for financial services. A credit union's member operation has two halves, the conversation on the frontline and the back-office case work behind it, and Gradient Labs is built to run both. Take a disputed transaction: the member raises it on the frontline, the investigation and chargeback work happen in the back office, and the outcome comes back to the member, all on one platform rather than handed across a gap between tools. That depth suits credit unions and community banks just as well as the fintechs and digital banks it grew up with, and it arrives without a long AI engineering project. Customers include Wise, Current, Rho, LHV Bank, Stash, Zego, and Pockit.

Security and compliance: every turn passes through 20+ pre-built financial-services guardrails, with regulatory coverage spanning the US (FDCPA, TCPA, Reg F, UDAAP), UK (FCA Consumer Duty, CONC, Breathing Space), and EU (GDPR, EU AI Act). SOC 2 Type II certification, AES-256 encryption, and zero-day retention agreements with every LLM sub-processor sit behind it, and the Vanta Trust Centre is public for due diligence.

Deployment: a non-technical ops lead can own the agent day to day, because the finserv-native delivery team handles the migration and absorbs the AI engineering. Expect 4 to 6 weeks to production for member service and back-office work; outbound collections is the exception, able to start calling from a CSV alone in under a day. Every scoped use case carries a money-back guarantee.

Resolution: 60% is the day-one norm; mature deployments run at 80-90%.

Honest limitation: transaction monitoring, credit decisioning, and loan origination sit outside its scope. The financial crime and lending agents below own those jobs; Gradient Labs runs the member operation next to them, and replaces none of them.

Best for: credit unions and community banks that need member services, disputes, and collections handled under examination-ready controls. See the Disputes Agent and the overdue payment collections use case for the named work.

"We truly think that if people have a problem and you solve it, that builds brand loyalty. That's why customer resolution is so important. With Gradient Labs, we have an AI agent that's actually resolving problems, boosting our CSAT rating, and absorbing growth without us having to scale the team. I'm confident that with this partnership, we can get to 100% automation."

Michiel Smet, Head of Operations, Pockit

Financial crime, fraud, and risk AI agents for credit unions

Credit unions carry the same BSA/AML obligations as banks and face the same examination scrutiny on suspicious activity reports, transaction monitoring, and KYC. The six agents in this section run that financial crime work behind the member-facing operation.

2. Sardine: best for fraud, AML, and compliance on one platform

Sardine puts fraud, AML, and compliance on one risk platform, and its newer agentic investigation work gathers evidence and interprets context across a case. The company has raised $145M to date, including a $70M Series C in 2025, and its 300+ customers include FIS, Deel, and GoDaddy.

Best for: credit unions consolidating fraud, AML, and compliance into a single risk platform.

3. Unit21: best for detection-to-investigation in one loop

Unit21's agentic fraud and AML platform covers the full loop from detection through investigation, with agents that show their working. It has raised around $92M, serves 200+ institutions (Intuit, Chime, and Sallie Mae among them), and earned a place on the 2026 RegTech100.

Best for: risk teams that want the alert and the investigation handled in the same system.

4. Hawk: best for explainable transaction monitoring

Hawk applies explainable AI to AML transaction monitoring and sanctions screening, drafting SARs automatically and cutting false positives. That explainability earns its keep at examination time, when someone asks why a monitoring decision fired and the answer has to hold. Munich-based Hawk raised a $56M Series C in 2025, bringing it to $83M total, and works with 80+ institutions.

Best for: replacing legacy transaction monitoring while keeping every decision auditable.

5. Lucinity: best for analyst-led investigations

Lucinity builds FinCrime investigation agents that cut casework from hours to minutes with the analyst still making the final call. Teams that want the speed without surrendering the judgement tend to land here. The Iceland-based company has raised $26M, and Pleo and Visa's Currencycloud are among its customers.

Best for: FinCrime desks that want faster investigations with analysts keeping the final say.

6. Norm Ai: best for operationalising regulation

Norm Ai turns laws, policies, and regulatory requirements into AI agents, so the judgement a regulation demands gets encoded into the compliance workflow itself. The distance between what a rule says and what an operations team actually checks is precisely the gap it closes. Investors including Coatue, Bain Capital, and Citi Ventures have backed it with over $140M.

Best for: compliance and legal teams that want regulatory requirements running as automated checks.

7. Oscilar: best for a unified risk layer

Oscilar covers fraud, AML compliance, credit risk, and onboarding from a single AI agent hub, and more than 100 financial institutions run on it. Founder Neha Narkhede co-created Apache Kafka; the company is bootstrapped with no outside funding, and SoFi, MoneyGram, and Nuvei are among its customers.

Best for: credit unions that want fraud, compliance, and credit risk decisioned in one layer.

Lending AI agents for credit unions

Auto loans, personal loans, SBA-backed business lending, and mortgages make up the core lending book at most credit unions. On the servicing side, Gradient Labs' own Lending Agent handles inbound queries, supports active borrowers, and secures promises to pay on accounts in arrears. Origination is a different job, and the two specialists below own it.

8. Casca: best for AI-native loan origination

Casca, built by Cascading AI, is an AI-native loan origination system in production at FDIC-insured banks and fintechs, strongest in small-business and SBA lending. Its $29M Series A was led by Canapi Ventures, taking total funding to $33M, and Live Oak Bank, Huntington National Bank, and Bankwell Bank are among its customers.

Best for: credit unions replacing manual business and SBA loan origination.

9. Parlay: best for widening the lending funnel

Parlay's loan-readiness agent works the top of the funnel, pre-qualifying and packaging SBA-focused applications so fewer of them stall before reaching a decision. Backed by JAM FINTOP at seed stage, it focuses squarely on community banks and credit unions that want more SBA volume.

Best for: credit unions growing SBA application volume without adding headcount.

How these agents fit together at a credit union

Before choosing anything, place each of the nine in one of three jobs. Sardine, Unit21, Hawk, Lucinity, Norm Ai, and Oscilar watch the money and the member for risk. Casca and Parlay carry a loan application through to a decision. Gradient Labs wraps the member-facing operation around both: the conversations members have, and the back-office cases those conversations trigger.

In practice the lines blur constantly: a flagged transaction turns into a member conversation, a personal loan in arrears turns into a hardship assessment, and a KYC review turns into a document chase with the member. Specialist decisioning belongs to the financial crime and lending agents; the member-facing operation, and the case work it generates, belongs to Gradient Labs. For the wider picture, see our AI in banking use case guide and our guide to the best secure AI agents for banking in 2026.

Which AI agent should your credit union choose?

You need member-facing and back-office operations run under FS-native guardrails: Gradient Labs.

You want to automate financial crime investigations: Sardine for fraud, AML, and compliance on one platform; Unit21 for detection and investigation in one loop.

You need transaction monitoring you can explain to an examiner: Hawk.

You want to speed up analysts without removing them: Lucinity.

You want regulation turned into automated checks: Norm Ai. For one risk layer spanning fraud, compliance, and credit, Oscilar.

You want to modernise lending: Casca for origination, Parlay for the top of the funnel.

To see the agent running one of your own member use cases, book a demo with Gradient Labs.

Emma Martin is the Head of Marketing at Gradient Labs. Prior to Gradient Labs, she held global marketing leadership roles at Bluecore (acquired by Insider One), Mastercard, and startups on the fronteir of conversational AI. She writes about the intersection of AI, automation and customer experience in financial services.