Nearly all banks have already run an AI pilot, usually starting with conversational AI for simple FAQs. Far fewer have managed to deploy AI agents in banking that work reliably on a daily basis, with real ROI. McKinsey found that 88% of organisations now use AI in at least one function, but only 39% see any EBIT impact, and the gap rarely comes down to the model. It comes down to deployment: the internal buy-in, the guardrails, the integrations, and the ramp up, all of which turn a promising demo into a beneficial system that risk and compliance will sign off on.

This guide breaks down how to deploy conversational AI agents in banking into six steps, in the order a traditional bank actually works through them, so your first deployment reaches production and your second one is easier.

1. Choose the right AI agent built for your banking use case

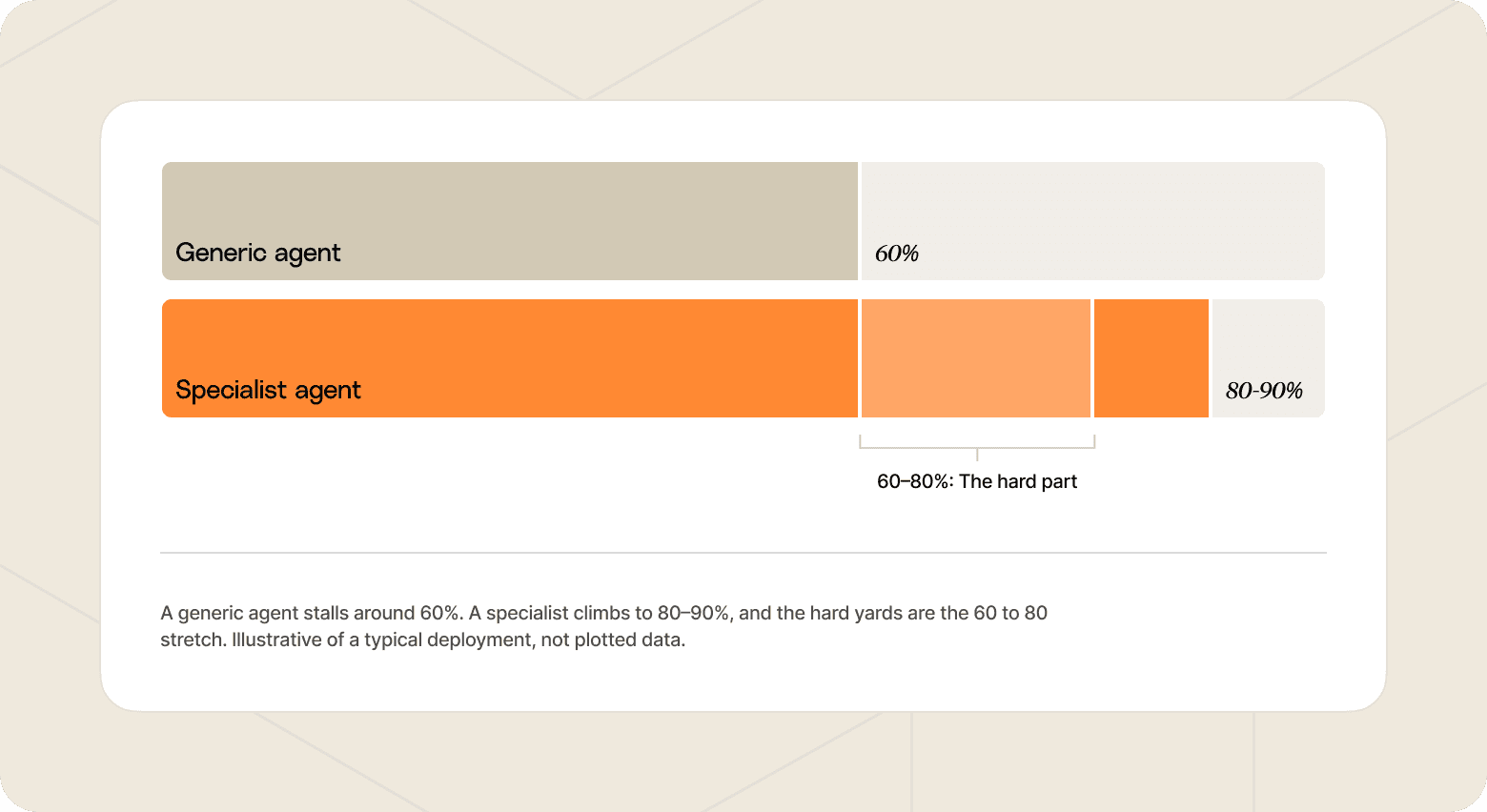

A generic conversational AI agent is built to answer a question and close the conversation. It handles things like "what's my ATM withdrawal limit?" or "how do I order a new card?" well enough, but it tends to plateau around 60% automation on a real banking operation, because most of a bank's manual customer operations don't fit the one question, one answer shape.

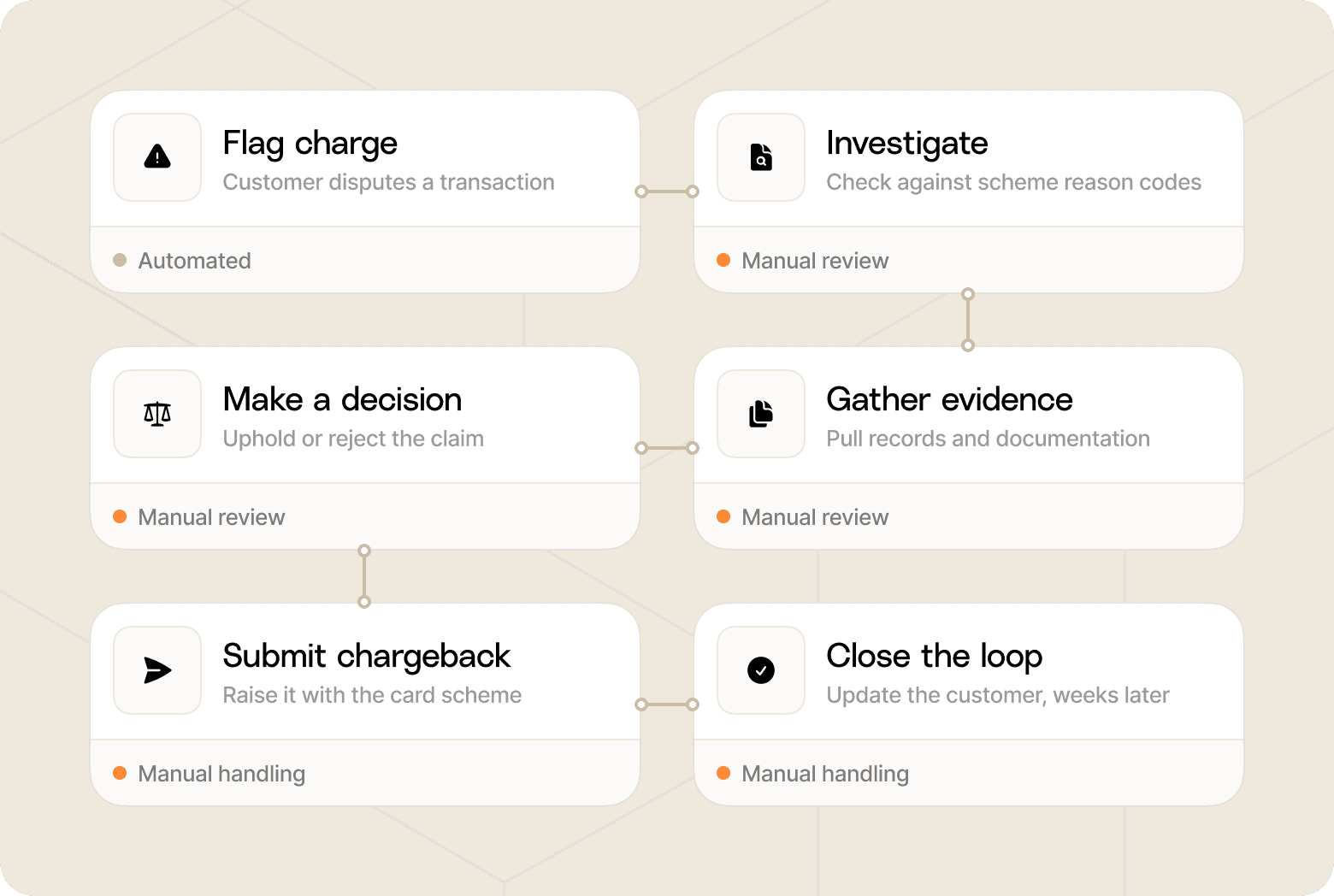

The work that defines a bank lives a layer deeper. For example, a disputed transaction requires more than a single reply. The customer flags a charge they don't recognise, the case goes into investigation against card scheme reason codes, evidence gets gathered, a decision gets made, the chargeback gets submitted, and someone closes the loop with the customer weeks later, all against the regulatory and scheme deadlines that govern disputes in every market you operate in.

Collections, complaints, bereavement, and financial vulnerability run the same way: long processes, not quick answers.

A specialised AI agent like Gradient Labs is better for banks on three fronts:

It runs the long process, not just the reply: Disputes, collections, KYC, complaints, and more require intake, investigation, decision, follow-up, and close. A specialist agent shares memory and context across every stage of that lifecycle. A generic agent's case stops at the first response.

Compliance is built in: In finance, a wrong answer can be a regulatory breach. Banks need specialist agents that run FS guardrails on every turn (complaint and vulnerability detection, tipping-off prevention, no unlicensed advice) with a full audit trail. Horizontal tools treat compliance as a configuration layer you build and maintain yourself.

It acts (securely) inside your systems: Resolving a case might require steps such as freezing a card, checking account status, or submitting a chargeback. A specialist agent connects to core banking, CRM, and case management to do the work, not just explain it.

Be critical about what kind of work you're automating and where an AI agent can have a real impact on your pain points. If it's first-line FAQ, most tools will cope. If it's the back-office work like disputes, collections, and KYC that actually impacts your operation, you need a specialised AI agent built for the process, not the reply. That depth is what lifts resolution past the ceiling that stalls generic agents, toward 80–90% in mature deployments.

This guide is focused on AI agents for customer operations in banking, but there are other use cases you might want to run, and you can read about them here.

2. Treat internal buy-in as the first step to deploying AI agents in banking

In a traditional bank, the agent has to pass your own people and processes before it ever reaches a customer. Risk, compliance, information security, and engineering each hold a veto, and procurement moves at its own pace. Treat the internal sell as the first deployment task, not a formality that follows it.

Three gates tend to decide it:

Security review: Your information security team assesses data handling, retention, encryption, and sub-processors against your own standards. Come with answers: SOC 2 and ISO 27001, GDPR with full DSAR handling, AES-256 at rest, and zero-day data retention agreements with every LLM sub-processor.

Compliance review: Risk and compliance check the agent against the regulations you live under, whether that's FCA Consumer Duty in the UK, Reg E and Reg Z in the US, or PSD2 and the EU AI Act in Europe. The audit trail matters here as much as the model does.

Prioritisation: Pick the first use case by impact, not by ease. Which SOPs and data connections unlock the most volume? That answer sets the order of everything that follows.

Then scope the proof-of-concept around one concrete question the agent must answer: can it find the customer, read the account status, and respond correctly under your guardrails?

One of Gradient Labs' customers, a US-based consumer investing platform deploying at scale, ran exactly this sequence in their deployment. They had a full security review and a tightly scoped pilot before a single live ticket. Gradient Labs guarantees the deployment once a use case is scoped: if we don't deliver what we agreed, you get your money back, which puts a floor under the decision for risk-averse stakeholders.

3. Teach the AI agent what your best people know

An AI agent knows what you give it, but a knowledge base on its own is never enough. Your best human agents in banking carry years of practised judgement that never made it into a document: the edge cases, the workarounds, the way a sensitive complaint actually gets handled. One of the first steps in a Gradient Labs deployment is getting that knowledge into the AI agent, and three sources feed it:

Knowledge base: Your help articles and policies, the documented baseline most human teams already have.

Facts: The structured details that don't live in a public knowledge base, like fee schedules, eligibility rules, and cut-off times. These are kept separate because they're precise and they change often.

Notes: Your team's working knowledge, the judgement that never got written down. This is the hardest source to capture by hand, so Gradient Labs generates it for you. The AI agent analyses thousands of conversations your team has already handled and extracts how your best people actually work: the recurring edge cases, the tone they use with a vulnerable customer, and the steps they take when a policy doesn't quite fit. Your team reviews what it surfaces, and it becomes guidance the agent applies from day one.

On top of knowledge sit procedures: your SOPs written as natural-language steps the agent executes, with branching logic for the cases that don't follow the script.

Because the agent learns from your real conversation history rather than a blank slate, it starts near your team's standard instead of climbing there through months of escalations. Treat early gaps the way you would with a new hire: a poor response signals missing context, not a dead end. You add the context, and the agent improves.

4. Ensure your AI agent understands banking regulations

In most industries, a wrong answer from an AI support agent means a poor customer experience. In banking, it can be a regulatory breach.

That raises the bar on what "working" means: the agent has to be controlled on every turn, and the controls have to be the platform's job, not a configuration layer your team builds and maintains.

At Gradient Labs, two kinds of guardrails do this work:

Customer guardrails read the conversation and act on it: detecting a complaint, spotting signs of financial difficulty or vulnerability that trigger consumer-protection obligations like FCA Consumer Duty in the UK, and rerouting or handing off when a human is needed.

Agent guardrails check what the agent is about to say or do: preventing tipping-off on a financial crime case, blocking unlicensed financial advice, and stopping sensitive data from leaving. They edit the draft before it reaches the customer.

Gradient Labs runs 20+ pre-built financial services guardrails on every turn, with coverage across US (FDCPA, TCPA, Reg E and Reg Z), UK (FCA Consumer Duty, CONC), and EU (PSD2, GDPR, the EU AI Act) rules. Every action, data point, and decision lands in an audit trail your risk and compliance teams can review. Horizontal tools treat this as the buyer's homework. For a regulated bank, that homework is the hard part, and it shouldn't be yours to do.

5. Safely integrate the AI agent with your banking systems

Answering a question and resolving a case are different jobs. The AI agent earns its return when it can act: freeze a card, check an account status, submit a claim, update a case. That means connecting it to the systems that actually run the bank, your core banking platform, your CRM, and your case management, through custom API tools rather than a sync with the help centre alone.

Sequence the integrations the same way you sequenced the use cases. Connect what unblocks your highest-priority case first, then widen. This is also where the economics turn. Much of the cost saving in AI programmes arrives past 80% automation, and the climb from 60% to 80% is the real work, most of it integration depth: every system the agent can reach is another case it closes without a human. Overdue payment collections is a plain example, since the agent can't resolve the case if it can't see the balance and take the payment.

Banks typically start with one narrow, high-volume process and add others on the same platform over time, reusing the same connections, guardrails, and audit trail for each new case.

6. Earn trust in the AI agent by starting with low-risk cases, then ramp

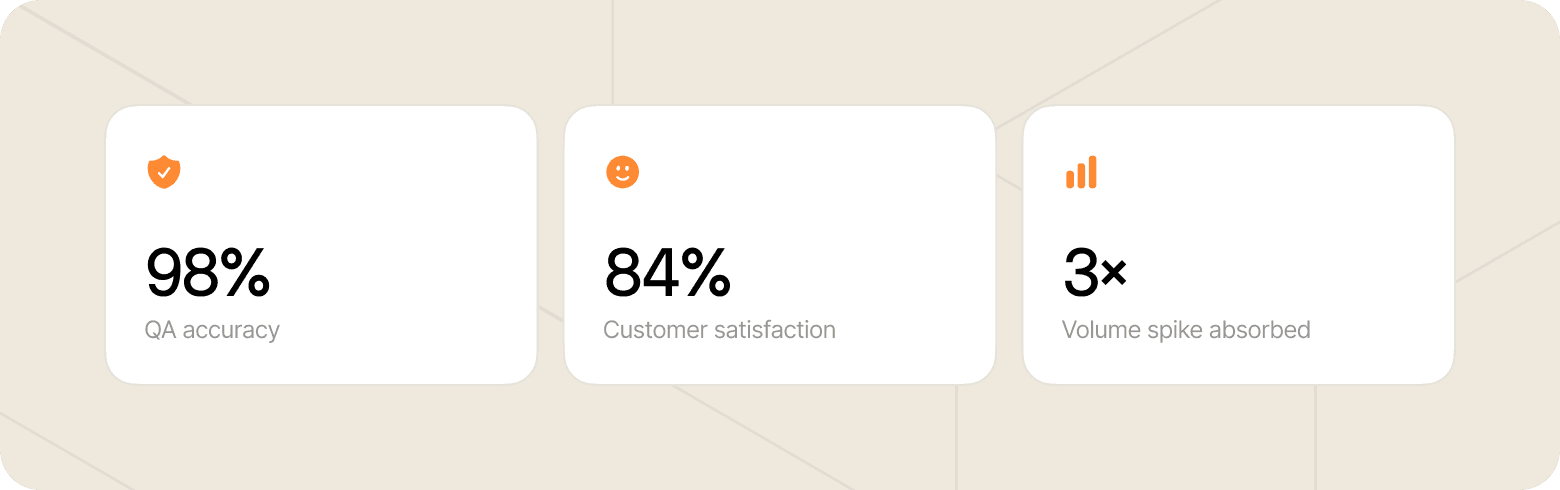

With so many stakeholders in a banking deployment, it's better to earn trust in increments, and a gradual ramp is how you build it. One of Gradient Labs' US customers started at 50 tickets a day with 100% human QA, then moved to 25%, 50%, and 100% of email volume as the numbers held, and never once rolled back. When 30,000 new accounts landed overnight and support volume tripled in a week, the AI agent absorbed it.

Going live is the start line, not the finish. A mature deployment reaches 80–90% resolution, but day one usually lands around 60%, and the gap closes through a maintenance loop you run after launch:

Watch the handoff rate: every handoff to a human is a case the agent didn't resolve.

Diagnose the root cause: missing knowledge, a gap in a procedure, or a missing integration.

Fix the source, then test and monitor: update the knowledge, procedure, or tool, validate it, and watch the rate move.

From there, growth runs on two axes: breadth (more channels, customers, and languages) and depth (more procedures, more tools, more of the case handled end to end). The customer-experience payoff compounds alongside. A large digital bank running Gradient Labs holds 98% QA across half a million conversations and an 84% CSAT, ahead of its human team. Done well, deploying AI agents in banking improves service quality and cost at the same time.

Deployment is the hard part, and it's the part Gradient Labs is built to carry: a banking-native platform, a delivery team that knows banking, and a guarantee on every use case we scope. If you're choosing where to start, our guide to AI use cases in banking maps the options, or book a demo and we'll plan your first deployment with you.